Tax Analysis of Shohei Ohtani’s Salary Deferral

As part of its ongoing effort to report on significant economic trends in California, the Center for Jobs and the Economy is releasing this special report, which provides a detailed analysis of Shohei Ohtani’s decision to defer most of his annual salary of $70 million over 10 years. It explores how this move might save Ohtani millions in taxes due to California’s highest-in-the-nation tax rate on high income earners and examines the wider impact on both the Dodgers’ finances and California’s revenue model. While other reports have attempted similar estimates, many have used the wrong tax rates or have not considered all the tax consequences. For additional information and data about the California economy visit www.centerforjobs.org/ca.

Table of Contents

- Ohtani Swings for the Fences and Dodges Curve Balls

- Tax Implications and Financial Offsets for the Dodgers

- High-Income Earners' Crucial Role in State Revenue Model

Ohtani Swings for the Fences and Dodges Curve Balls

Shohei Ohtani’s new contract with the Dodgers is worth $70 million a year for 10 years, but he will get only $2 million a year while deferring the remaining $68 million to the following decade. In the interim, Ohtani will have to make do with his additional endorsement income of at least $40 million a year, assuming some of that is not deferred as well.

Who gets to tax the deferred income will depend on Ohtani’s official residence when the payments are actually made. If paid up front, the full $70 million would be subject to California’s highest-in-the-nation 13.3% income tax rate plus an additional 1.1% based on the stealth-expansion of the California State Disability Insurance tax rate. Deferring the $68 million a year likely enables this tax bite to be avoided altogether.

To estimate the potential savings to Ohtani, we ran the numbers using the National Bureau of Economic Research TAXSIM model. The numbers assume: (1) only the Dodgers payments are covered as income, with endorsement and any other income put to one side, (2) payments are made to him directly rather than a holding company or some other business entity, (3) no additional deductions (e.g., mortgage, other interest, holding company expenses), and (4) Ohtani remains single, an issue of enduring fascination and speculation in the sports press. The TAXSIM runs are done using the estimated 2023 rates, although the actual tax rates will be subject to change over the 20-year period. The results are in the table:

While the federal tax savings of $27.4 million a year will eventually have to be paid once the deferred payments start kicking in—although, again, at somewhat different rates as the tax brackets are adjusted due to inflation and possibly future Congressional action—the California share of the tax take likely can be avoided altogether depending on his official residence at that point in time. Deferring the income potentially saves Ohtani an additional $9.8 million annually in taxes, or $98 million over the life of his contract.

Tax Implications and Financial Offsets for the Dodgers

There are some offsetting increases to the Dodger’s tax bill in this period. Ignoring the time value of money, increases in annual tax liability to the state due to lower costs (salary and payroll taxes) in the first 10 years will be offset by decreases in the next 10 as the deferred payments are made. However, the deferral also likely avoids triggering Major League Baseball’s luxury tax. Assuming the full contract is valued at $46 million a year under the MLB rules, the Dodgers could be subject to an average luxury tax of up to an additional $10.8 million a year if the contract was paid out directly with no deferrals. The LA Dodgers are structured as an LLC. Assuming it is taxed at C Corp rates to simplify the calculations, dodging the MLB luxury tax could increase their corporate tax liability by up to an additional $955,000 a year.

High-Income Earners' Crucial Role in State Revenue Model

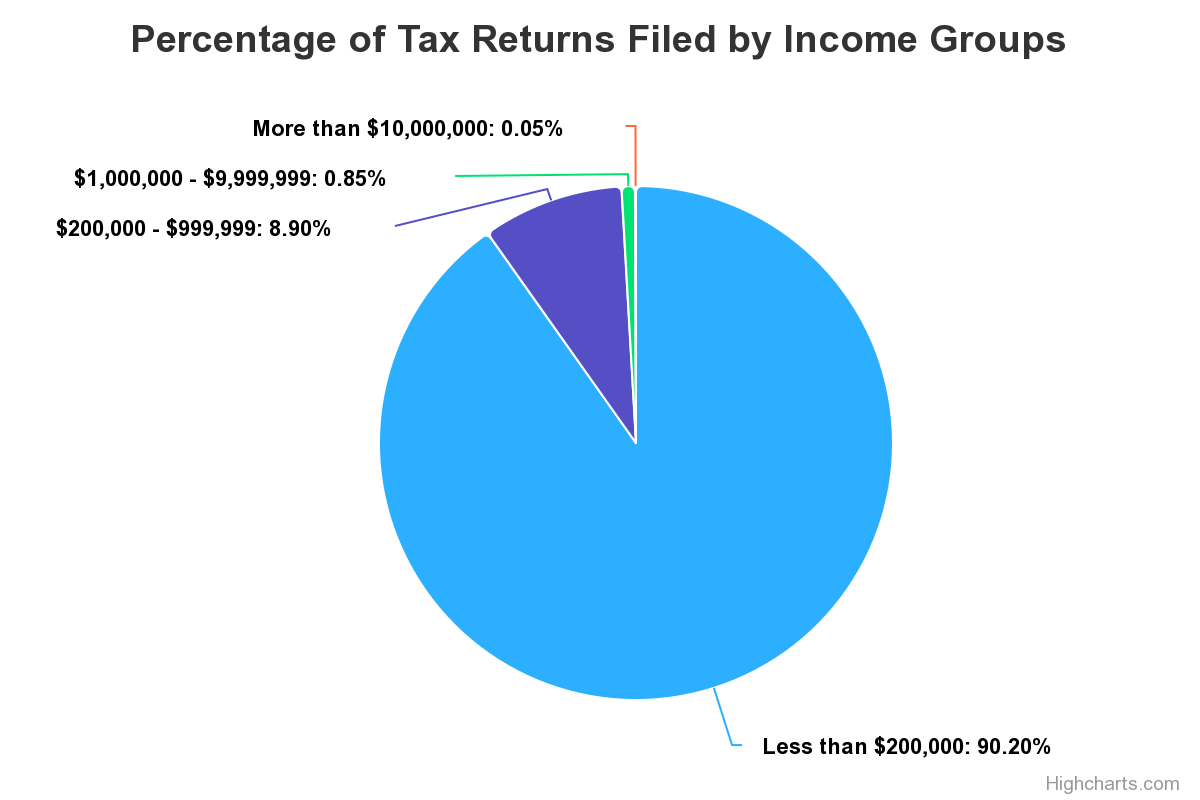

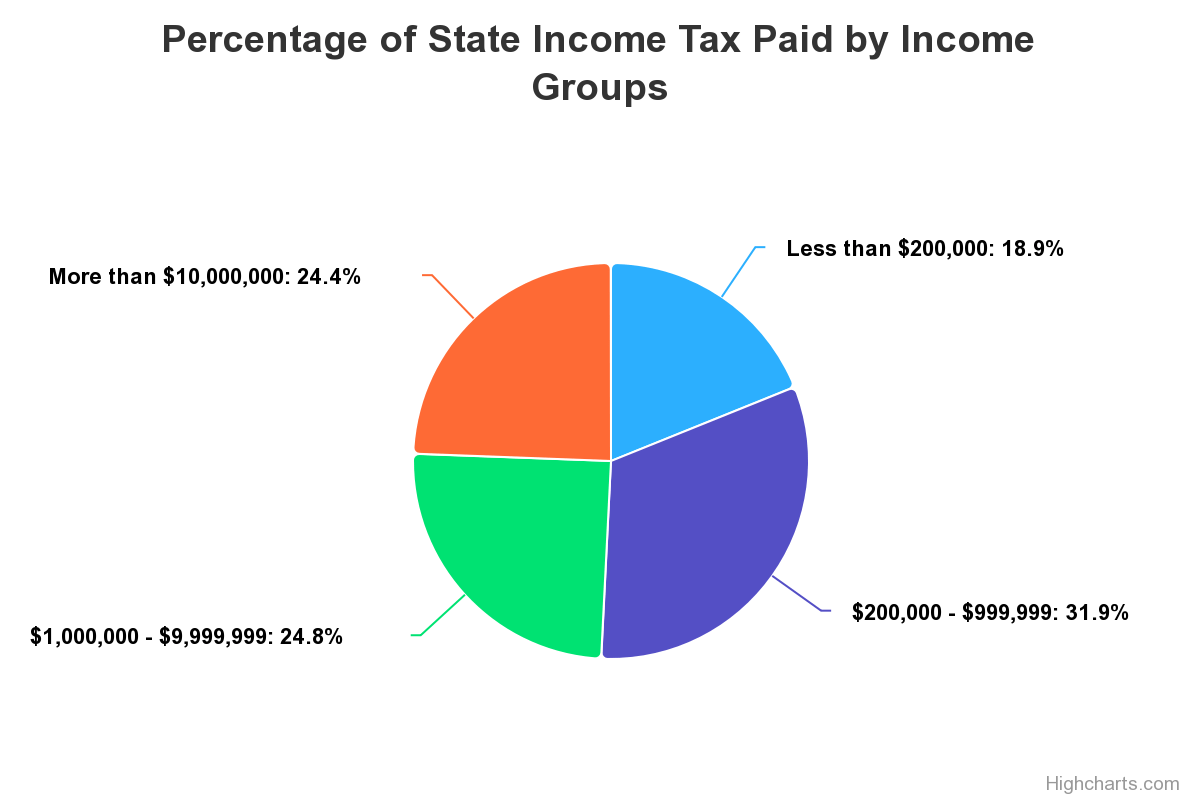

California’s budget revenue model depends heavily on high income taxpayers like Ohtani, and more importantly relies on both their income and their residency staying in the state. In the latest 2021 results from the Franchise Tax Board, these high-income earners—defined by Internal Revenue Service as taxpayers with adjusted gross income (AGI) of $200,000 or more—comprised only 9.8% of all tax returns. However, this group paid 81.1% of the total personal income tax. To break this down further, high earners with AGI of $1 million or more accounted for only 0.9% of all tax returns but paid nearly half (49.2%) of the total tax. An even smaller group, high earners with AGI of $10 million or more, constituted only 0.05% (8,519) returns but paid just under a quarter (24.4%) of the total tax.

The state’s tax system leans significantly on these few taxpayers. For instance, the amount of income tax Ohtani could save annually by changing his residence in 2033 is equivalent to the total tax liability of the bottom 1.78 million tax filers in 2021 (positive AGI). To use another illustration, finding just 317 more individuals like Ohtani (with no deferrals and MLB approval for the 12 required expansion teams) or doubling the taxes paid by the bottom 3.34 million tax filers could erase the state’s projected deficit for 2024-25.

While the looming deficit now being projected for the state budget comes in part from the weakening state economy, migration of the extraordinarily small taxpaying base likely is contributing as well.