The latest new vehicle sales data from California New Car Dealers Association indicates that new vehicle sales remain on track again to exceed 2 million for the year, even though Q2 sales were down slightly by 0.7% compared to the same quarter in 2017. Q2 sales for battery electric plug-ins (BEVs) were up primarily as a result of Tesla finally fulfilling earlier reservations for Model 3. Total PEV sales (plug-in hybrids and BEVs) were up due to this result and the continued shift from standard hybrid to PEV sales. Key findings from the data:

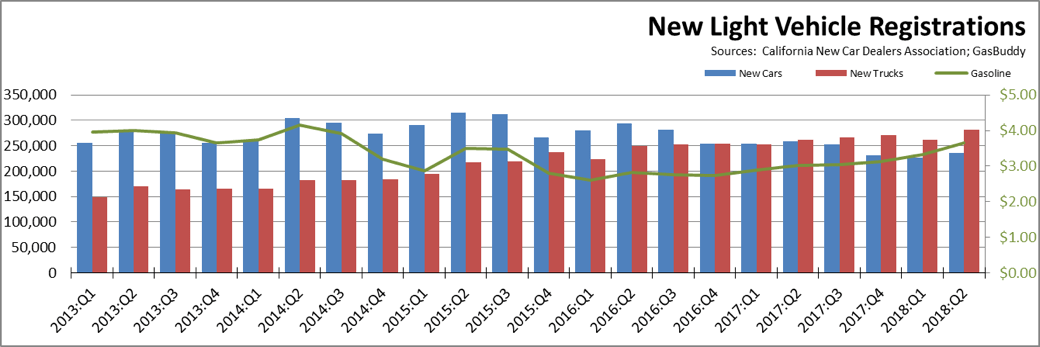

Light Trucks Sales Share Up to 55% of Sales

-

- Light truck market share was 55.5%, up from 50.4% in Q2 2017. The growing consumer preference for larger vehicles continues to be a contra-trend affecting the state’s ability to achieve its ZEV goals, as fewer models are available in this market component at price points that would achieve broader sales. The few models that are now offered in this class tend to be in the high end of the market.

- Consumer shifts to light trucks for the US outside California was even more pronounced, accounting for 69.6% of new light vehicle sales in this quarter. The potential for California’s ZEV policies to have much of an effect beyond its borders are increasingly limited as a consequence, as few models are being offered for the types of vehicles consumers prefer to buy.

- The trend towards light trucks came even in spite of higher fuel prices. The average California price for regular gas in Q2 2018 was $3.66 a gallon, 21.0% higher than the prior year’s $3.03.

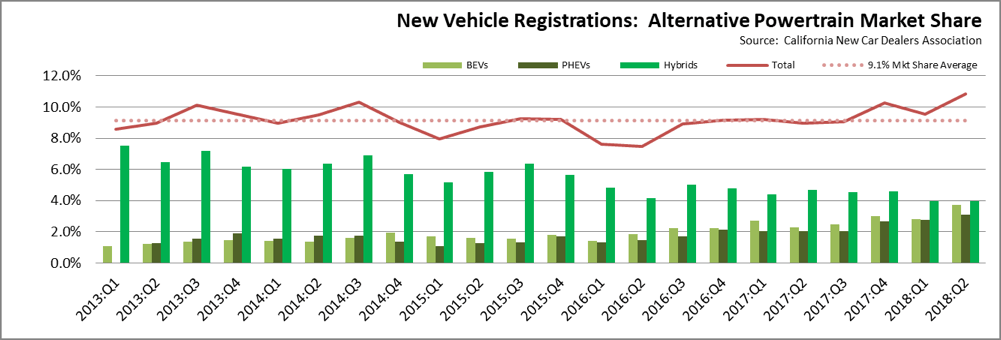

PEV Sales Up in Second Quarter

- 2018:Q2 PEV sales (plug-in hybrids and battery electric vehicles) at 35,466 vehicles, up from 22,427 in 2017:Q2 and up by 8,255 from 2017:Q4. Total market share for PEVs was 6.9%, up from 4.3% in 2017:Q2.

- True zero emission sales (battery electric vehicles) at 19,358 vehicles, up from 11,828 in 2017:Q2 and 13,657 in the prior quarter, with market share going from 2.3% in 2017:Q2 to 3.7% in 2018:Q2.

- Standard hybrid sales (HEVs except for plug-in hybrids) at 20,595, down from 24,321 in 2017:Q2. Total market share was 4.0%, down from 4.7% in 2017:Q2 but the same as 2018:Q1.

- The growth in PEV sales share in this quarter is the result of two key factors:

- Most PEV sales continue to come as consumers otherwise open to an alternative fuel vehicle shift to plug-ins rather than buying a standard hybrid. As shown in the chart below, total market share for all alternative powertrains (BEV, PHEV, HEV) has deviated little from the long term average of 9.1%. The only significant differences: (1) 2017:Q4 saw a 10.2% share but was likely driven by consumers’ expectations—driven in turn by dealers’ advertising—of a possible subsidy cut in the federal tax reform bill, a likelihood that is illustrated by a dip in the following quarter; and (2) 2018:Q2 which was affected heavily by the next factor below.

- Tesla finally began significant shipments of Model 3 from prior orders. Tesla’s sales in California were up 9,815 from 2017:Q2, of which 8,951 were Model 3 shipments for orders posted in the prior year. These sales may indicate that a break from the 9.1% long term market share may finally be taking place, but more than one quarter of data and sales generated by current rather than prior-year consumer decisions will be needed to show a change in this trend. Counter to previous expectations that Model 3 would finally represent a break-through in BEV prices that would open up electric vehicles to a wider market, current deliveries are at a price point that keeps this model in the near luxury category, limiting its future ability to appeal to a wider segment of the market.

- The future direction for PEV sales is also uncertain as a result of a looming shift in the subsidies available to buyers of these vehicles. As indicated by prior experiences in Denmark, the Netherlands, and—within the US—Georgia, PEV sales are highly sensitive to changes in these subsidies. California has already made substantial cuts to the availability of its rebates by imposing income limits for eligibility. Tesla appears to have breached the total sales threshold for its models to be eligible for federal rebates, and GM appears to be few quarters away, with Nissan at 60% and Ford at 55% of the cap[1]. Once the cap is reached, federal subsidies are phased out over the following two quarters.

While these more public subsidy sources are declining, ZEV producers also have available subsidy revenues as the result of selling regulatory credits, both for compliance with the ZEV rules in California and the other adopting states and under the federal fleet fuel efficiency standards. While shifting the subsidy cost incidence from government budgets to those consumers buying traditional fuel vehicles, the associated scale was also likely set to increase under rules made final in the last few days of the Obama Administration. While these regulatory credits will still retain considerable value as a subsidy source even under the recently proposed rule revisions, there is likely to be a period of uncertainty until the rules are finalized and the announced litigation is eventually resolved.

Consequently, the current quarter sales results are too premature to determine whether a longer term shift in consumer acceptance is taking place that would broaden the market share for these vehicles. This outcome will not likely become known until additional quarters’ worth of data becomes available from sales as ZEV producers set pricing closer to the costs of production as both the state and federal subsidies subside.

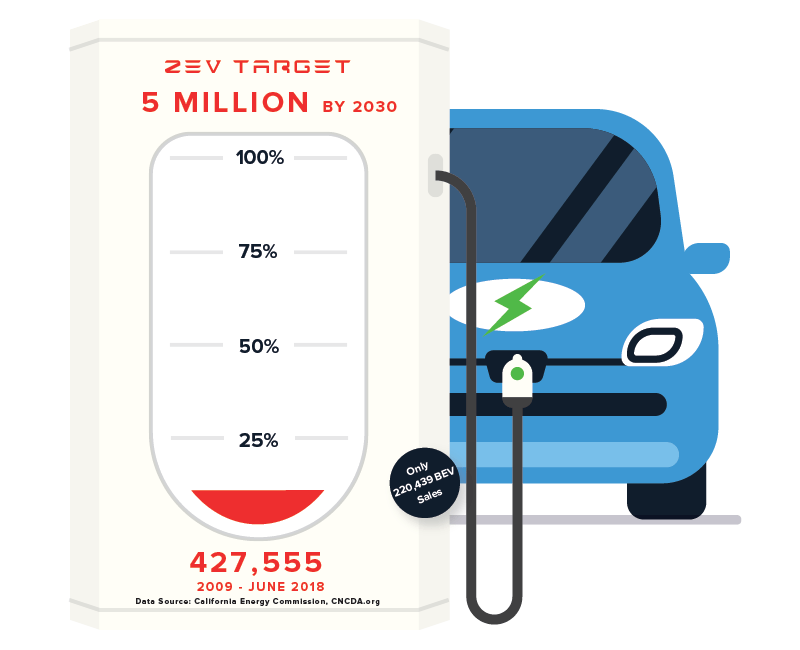

Cumulative PEV Sales at 8.6% of 2030 Goal—True ZEVs at 4.4%

As part of the AB 32 climate change program, Executive Order B-48-18 administratively created a goal of 5 million zero-emission vehicles (ZEVs) on California roads by 2030. This action expands on the prior Executive Order B-16-2012, which set a goal of 1.5 million by 2025, with a sub-goal that their market share is expanding at that point. While these goals were set administratively, they are reflected in the state’s climate change strategies, and both public and utility ratepayer funds are being used to create the refueling infrastructure required for these motorists.

Rather than only true ZEVs, the numbers in the Executive Order and previous interpretations by the agencies indicate the goal is to be achieved by both BEVs that run only on electricity and plug-in hybrids (PHEV) which run on both electricity and motor fuels. Consequently, only a portion of the vehicles being counted to meet the zero emission goal—roughly half based on current sales volumes—will in fact produce zero emissions. Additionally, FCEVs (fuel cell electric vehicles) also would count towards the ZEV total, but CNCDA data show total market share for these vehicles to date at only 0.1%.

Using this more flexible interpretation, total PEV sales since 2009 account for 8.6% of the 2030 goal. True ZEV sales (BEVs), however, account for only 4.4%.

The Executive Orders, however, also refer to ZEVs on California roads, while the agency accountings concentrate on sales. Using prior Energy Commission reviews to account for ZEVs no longer on the roads as a results of accidents, moves out of state, and other factors that over time remove vehicles from the active fleet, the actual progress rate consistent with the Executive Order language of “vehicles on California’s roads” would be 7.9% rather than the 8.6% shown in the chart below.

Accounting for normal fleet turnover rates and reductions from persons moving out of California, PEV sales would need to be 3.9 times higher to meet the 2030 goal. True ZEV sales would have to be 7.8 times higher. These calculations, however, incorporate the significantly higher Tesla sales in the current quarter as discussed above.

Manufacturing Job Provisions of Executive Order B-16-2012 Still Not Implemented

Like its predecessor, Executive Order B-48-18 contains some language referencing the economic and jobs potential associated with expansion of the ZEV market in California. However, the primary language shows a shift in focus to developing temporary construction jobs through installation of charging infrastructure rather than the permanent manufacturing and associated jobs development originally envisioned in B-16-2012. However, because this earlier order was not repealed, its provisions would still remain in effect.

Executive Order B-16-2012 contains a number of provisions calling for actions to expand the ZEV and ZEV component manufacturing base in California:

- [By 2015] The State’s manufacturing sector will be expanding zero-emission vehicle and component manufacturing;

- [By 2020] The private sector’s role in the supply chain for zero-emission vehicle component development and manufacturing State will be expanding.

- [By 2025] The zero-emission vehicle industry will be a strong and sustainable part of California’s economy;

The state’s current energy costs, additional labor law restrictions and litigation risks, and lengthy permitting processes continue to limit the ZEV related manufacturers choosing to locate within California. Rather than tackle these well-documented barriers to new manufacturing jobs, the most recent version of the ZEV Action Plan instead calls primarily for data collection and conversations:

Moving forward, state government will play a central role connecting regions to share best practices, gathering economic data to measure ZEV market growth and ensuring our workforce is trained to meet future needs.

Since the last update, Tesla’s Fremont facility continues to be the primary ZEV producing presence in California, with the battery components—which typically comprise half the value chain of an electric vehicle—produced in the Nevada Gigafactory. Other related announcements since the last quarter include:

- At the Beijing Motor Show in April, Toyota committed to “pioneer electric vehicles here [China],” with PHEV versions of the Corolla and Levin to begin next year and BEV production planned to begin in 2020. Other automakers highlighted progress on prior agreements including Nissan’s expectations to begin shipments from their China production in the second half of 2018, Honda’s joint ventures GAC Honda Automobile and Dongfeng Honda Automobile, BMW’s release of the iX3 SUV electric model in China, Volkswagen’s production at six plants in China by 2021, Chinese-owned Volvo’s plans for BEVs to comprise 50% of its sales by 2025, and Tesla’s plans to take a majority stake in a Chinese company to strengthen its presence in the country.

- While China announced it would gradually ease rules requiring 50-50 ventures with local companies, most European and North American automakers at the Beijing Show indicated they would rely local partnerships to comply with China’s electric vehicle rules.

- Canada’s Magna International announced a joint venture with a BAIC subsidiary to engineer and build two premium models in China.

- GM and Honda signed an agreement to development EV batteries to be produced at GM’s Michigan plants.

- Chinese-owned Byton announced raising $500 million to begin vehicle production in 2019. R&D center is in Silicon Valley, design center is in Germany, but manufacturing is set for Nanjing.

- SF Motors released details for production at its Indiana plant, including $160 million investments and an expected 467 jobs.

- German trade unions in conjunction with automakers released a study projecting a loss of 75,000 union jobs as a result to producing 25% BEVs and 15% PHEVs at German auto plants by 2030. With fewer parts, the new vehicles will require fewer workers to produce.

- Nio acquired more space for its operations in San Jose. San Jose remains the company’s software development center, but manufacturing is located in Shanghai.