The latest new vehicle sales data from California New Car Dealers Association indicates that while still projected to be at the fourth highest level during the past 11 years, new vehicle sales in California are now expected to be just shy of 2 million for the year. Q3 deliveries for battery electric plug-ins (BEVs) continued to be up primarily as a result of Tesla fulfilling reservations for Model 3 made in prior quarters beginning in 2017. Total PEV sales (plug-in hybrids and BEVs) were up due to this factor and the continued shift from standard hybrid to PEV sales. Key findings from the data:

Light Trucks at 55% of Sales

-

- Light truck market share was 55.5%, up from 51.3% in Q2 2017, as consumers continue to show a preference for this type of vehicle.

- Consumer shifts to light trucks for the US outside California was even more pronounced, accounting for 71.3% of new light vehicle sales in this quarter. The potential for California’s ZEV policies to be replicated beyond its borders remains low as the market segment targeted by most PEV models—cars—continues to contract as a result of consumer preferences. This trend is evident in GM’s recent announcement on the likely closing of three plants producing sedans (including the Volt PHEV) in order to move the company’s focus more to the light trucks/SUVs/crossovers consumers are buying as well as electric vehicles—which produce the credits needed to stay in compliance with both CAFE and ZEV regulations while enabling continued sales of the more profitable light truck models. This action follows on similar but earlier moves by Ford and Fiat Chrysler.

- The trend towards light trucks continues in spite of higher fuel prices. The average California price for regular gas in Q3 2018 was $3.64 a gallon, 19.5% higher than the prior year’s $3.05.

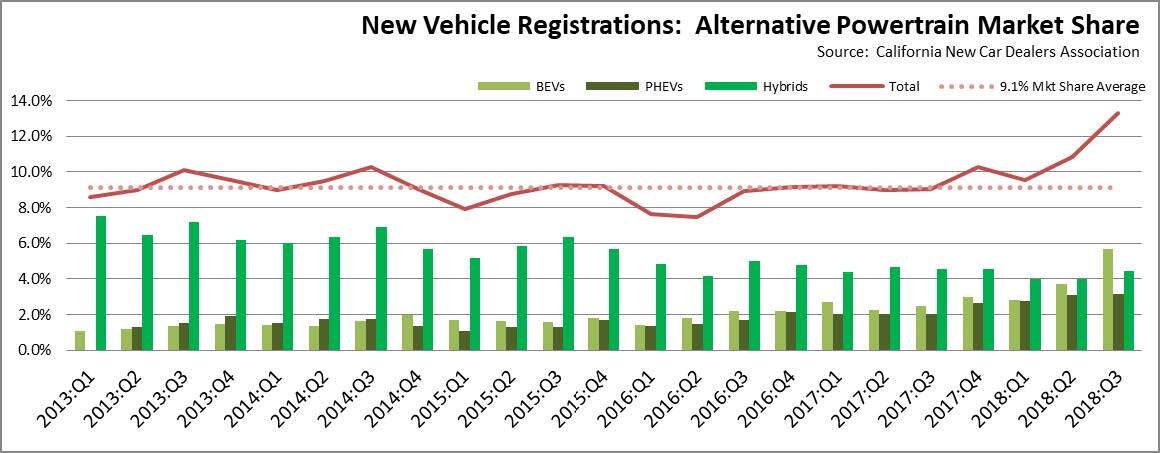

PEV Sales Up in 3rd Quarter

| 2018:Q3 | 2017:Q3 | |||

|---|---|---|---|---|

| number | mkt share | number | mkt share | |

| BEV | 28,371 | 5.7% | 12,796 | 2.5% |

| PHEV | 15,915 | 3.2% | 10,540 | 2.0% |

| PEV | 44,286 | 8.9% | 23,336 | 4.5% |

| HEV | 22.178 | 4.4% | 23,611 | 4.6% |

| Total | 66,464 | 13.3% | 46,947 | 9.1% |

Source: Derived from California New Car Dealers Association

- BEV sales saw a substantial increase (from 2.5% to 5.7% share of total sales), but primarily as a result of Tesla’s escalating delivery of vehicles from sales essentially made in prior quarters beginning in summer 2017. Tesla sales volume in this quarter was 22,758 (all models), or 80% of all BEVs sold in the state. While the BEV component is likely to continue rising in the next few quarters as Tesla continues to ramp up production to deliver on its backlog of order deposits, the longer term market penetration of BEVs will not become clear until sales conditions work through this current extraneous factor affecting the data. Tesla stopped taking reservations in July 2018 and has since moved to a direct order system, a change that will bring the data closer to its actual trend in the coming quarters.

- PHEV sales continued to rise, but only 11% above the prior three-quarter average, offset partially by a dip in HEVs compared to the year prior.

Alternative Market Share Above Long-term Trend

- Over the longer term, sales of alternative fuel vehicles have deviated little from an average market share of 9.1%. The sales mix instead has changed as consumers open to these vehicles have shifted from HEVs to PEVs as more models have become available. The latest quarter instead shows a rise to a 13.3% market share, but primarily as a result of Tesla accelerating deliveries on its Model 3 order backlog. As these backlog deliveries even out and Tesla sales better reflect current direct orders, the resulting effect on the ongoing market share will depend on a number of factors:

- Model 3 originally was envisioned as break-through in BEV prices opening up electric vehicles to a broader market, with a target base price of $35,000 on the most affordable configuration. This option, however, was removed from the Tesla website at least as early as mid-July 2017, [1] with current deliveries for configurations beginning at $46,000, rising to $72,500. The Tesla website does show models with prices at $31,700, but this amount incorporates potential rebates (at a level not available to all buyers) and estimated lifetime gas savings (which will vary by location, driving patterns, future gas and electricity prices, and other factors). A longer term expansion of market share will still require BEV models at prices that expand the market beyond its historic higher income base. [1]

- Tesla has reached its sales cap for the purposes of federal tax credit eligibility, and California previously limited the comparable state rebates by instituting household income restrictions. While Tesla sales in the 4th quarter are still likely to be elevated in part due to continuing backorder delivery, additional one-time bumps are likely to occur due to warnings on the company website advising potential buyers to “Order by November 30th to ensure eligibility for the $7,500 Federal Tax Credit. Tesla will expedite shipping for 2018 delivery.” GM is likely to breach the cap in 2018, with Toyota, Nissan, and Ford on track to do so as well in the next 4 years. The effects due to rising prices as the credits are phased out remain to be seen.

- Additional pricing uncertainty for Tesla and other PEV models stems from the continuing dispute between California and the federal government over the state’s ZEV waiver and proposed amendments to the CAFE regulations. Tesla’s most recent 10-Q for the 3rd Quarter indicates the company earned $189.5 million from the sale of credits generated by these regulations, or an additional credit of $2,260 per vehicle sold. The current versions of the waiver and regulations are structured to increase the value of these credit sales over time and provide at least some offset to the expiring tax credits—while shifting the cost burden from general taxes to consumers buying traditional fuel vehicles.

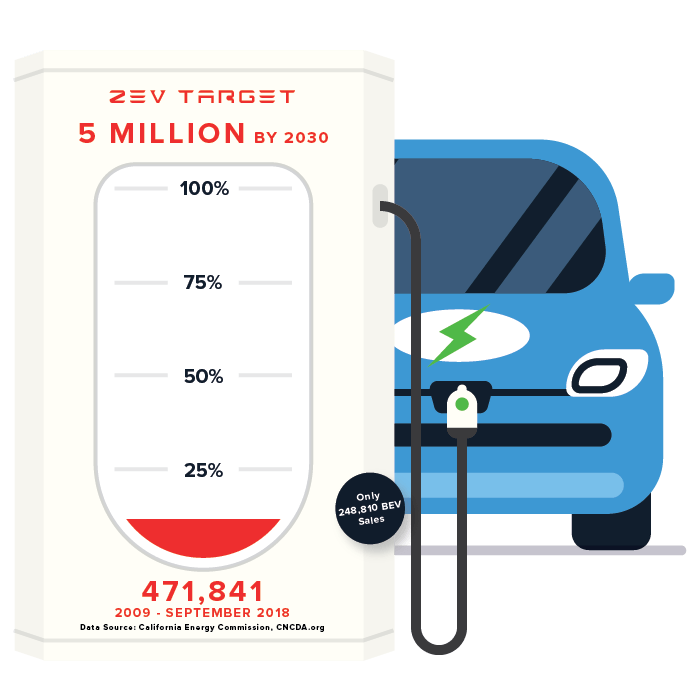

Cumulative PEV Sales at 9.4% of 2030 Goal—True ZEVs at 5.0%

As part of the AB 32 climate change program, Executive Order B-48-18 administratively created a goal of 5 million zero-emission vehicles (ZEVs) on California roads by 2030. This action expands on the prior Executive Order B-16-2012, which set a goal of 1.5 million by 2025, with a sub-goal that their market share is expanding at that point. While these goals were set administratively, they are reflected in the state’s climate change strategies, and both public and utility ratepayer funds are being used to create the refueling infrastructure required for these motorists.

Rather than only true ZEVs, the numbers in the Executive Order and previous interpretations by the agencies indicate the goal is to be achieved by both BEVs that run only on electricity and plug-in hybrids (PHEV) which run on both electricity and motor fuels. Consequently, only a portion of the vehicles being counted to meet the zero emission goal—roughly half based on current sales volumes—will in fact produce zero emissions. Additionally, FCEVs (fuel cell electric vehicles) also would count towards the ZEV total, but CNCDA data show total market share for these vehicles to date at only 0.1%.

Using this more flexible interpretation that includes both true ZEVs and combustion PHEVs, total PEV sales since 2009 account for 9.4% of the 2030 goal. True ZEV sales, however, account for only 5.0%.

The Executive Orders, however, also refer to ZEVs on California roads, while the agency accountings concentrate on sales. Using prior Energy Commission reviews to account for ZEVs no longer on the roads as a results of accidents, moves out of state, and other factors that over time remove vehicles from the active fleet, the actual progress rate consistent with the Executive Order language of “vehicles on California’s roads” would be 8.7% rather than the 9.4% shown in the chart below.

Accounting for normal fleet turnover rates and reductions from persons moving out of California, PEV sales would need to be 3.3 times higher to meet the 2030 goal. True ZEV sales would have to be 6.1 times higher. These calculations, however, incorporate the significantly higher Tesla sales in the current and previous quarters as discussed above.

Manufacturing Job Provisions of Executive Order B-16-2012 Still Not Implemented

Like its predecessor, Executive Order B-48-18 contains some language referencing the economic and jobs potential associated with expansion of the ZEV market in California. However, the primary language shows a shift in focus to developing temporary construction jobs through installation of charging infrastructure rather than the permanent manufacturing and associated jobs development originally envisioned in B-16-2012. However, because this earlier order was not repealed, its provisions would still remain in effect.

Executive Order B-16-2012 contains a number of provisions calling for actions to expand the ZEV and ZEV component manufacturing base in California:

- [By 2015] The State’s manufacturing sector will be expanding zero-emission vehicle and component manufacturing;

- [By 2020] The private sector’s role in the supply chain for zero-emission vehicle component development and manufacturing State will be expanding.

- [By 2025] The zero-emission vehicle industry will be a strong and sustainable part of California’s economy;

The state’s current energy costs, additional labor law restrictions and litigation risks, and lengthy permitting processes continue to limit the ZEV related manufacturers choosing to locate within California. Rather than tackle these well-documented barriers to new manufacturing jobs, the most recent version of the ZEV Action Plan instead calls primarily for data collection and conversations:

Moving forward, state government will play a central role connecting regions to share best practices, gathering economic data to measure ZEV market growth and ensuring our workforce is trained to meet future needs.

Since the last update, Tesla’s Fremont facility continues to be the primary ZEV producing presence in California, with the battery components—which typically comprise half the value chain of an electric vehicle—produced in the Nevada Gigafactory. Other related announcements since the last quarter include:

- Rivian premiered its electric pick-up at the Los Angeles Auto Show. Production will be in Illinois.

- Dyson announced it will build its production facility in Singapore.

- Samsung announced its first US automotive battery pack manufacturing facility will be located in Michigan.

- SK Innovation announced a $1.67 billion automotive battery facility near Atlanta, GA.

- Mercedes-Benz broke ground on an automotive battery plant in Alabama. This facility will support the company’s intended production of electric vehicles at its Tuscaloosa facility.

[1]“Tesla Removes Affordable Model 3 Variant from Website,” GM Authority, July 17, 2018.