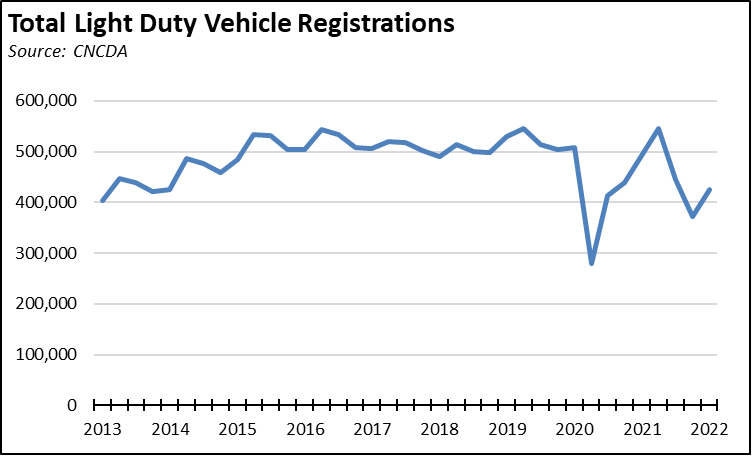

In the latest report from California New Car Dealers Association (CNCDA), total new light-duty vehicle registrations in the first quarter of 2022 were off 13.8% from the same period in 2021, and 19.8% below the same period in pre-pandemic 2019. Total sales for the year are expected to be just slightly higher than the 1.86 million seen in 2021. Rather than demand, however, the limiting factor is expected to be production as supply chain and labor shortages continue to be the dominant factors over the remainder of the year. Viewed on a quarterly basis, new registrations continue to be far more variable than in the pre-pandemic period.

Light Trucks Continue to Dominate New Vehicle Sales—Average Vehicle Price up 13.0% Over Year

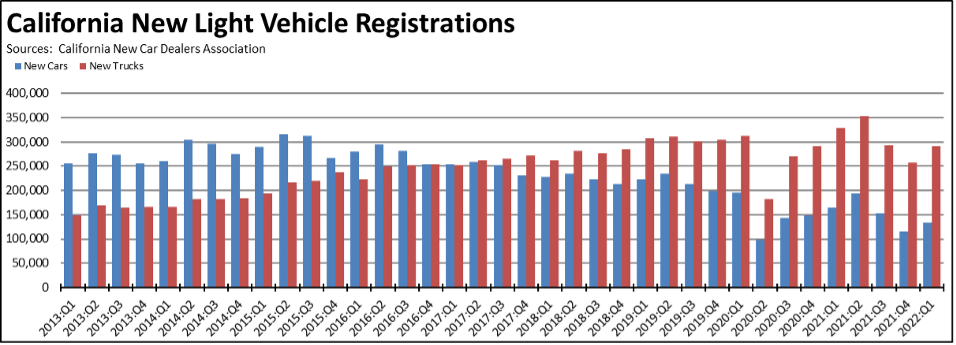

Consumer preferences continued to trend towards light trucks. In California, light trucks were little changed at 68.6% of total sales in Q1 2022. Sales in the rest of the US notched up to 81.1% for the quarter.

As with total sales, however, the currently elevated shares for light trucks just as likely reflect production decisions as consumer tastes. Light trucks in general are higher margin models providing the bulk of producer profits required to stay in business and support the new rounds of investments now required by mandates such as California’s pending Advanced Clean Car rule and the federal tightening of the CAFÉ fuel efficiency standards. Faced with shortages in parts and components, producers are now giving priority to the higher margin lines along with models required for regulatory compliance. In the process, however, average new car prices continue to climb, dragging average used car prices up as well as they rise.

In the latest report from Kelley Blue Book, the average transaction price nationally for new vehicles rose again in April to $46,526, up 13.0% over the year. Price increases varied widely by vehicle class, with the strongest jump of 27.2% to $38,335 for Hybrid/Alternative Energy Cars. Electric Vehicles saw the fourth highest average price rise at 16.1% to $65,111. The smallest increase at only 1.4%—reflecting a price decrease in real terms—was for Small/Mid-size Pickup Trucks ($39,783).

ZEV Sales Up 55.4% from 2021: Q1

New registrations of battery vehicles were up in the 1st quarter, although potential sales continued to be affected by the production halt of GM’s models. Recalls of GM’s Bolt were first announced in November 2020, and production was subsequently put on hold until the first week of this April while issues related to battery fire potential were resolved—a problem that cropped up even though the Bolt specifically and GM in general have by far the longest development period of any electric vehicle producer on the road today, beginning with the Electrovair I concept car in 1965 and initially culminating in the EV1 as the first production ZEV in 1996.

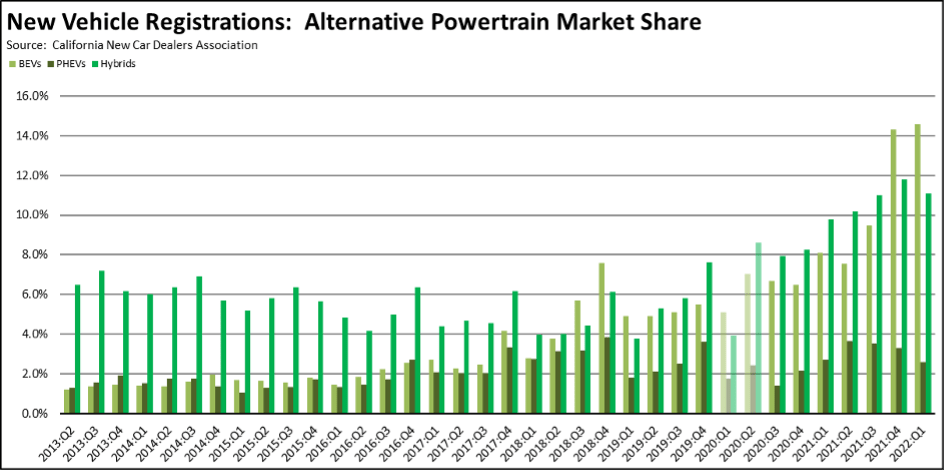

Sales of true ZEVs (battery electric vehicles—BEVs) rose 55.4% over the year largely on production from Tesla which comprised 77% of the total. The more volatile combustion engine component—plug-in hybrids (PHEV)—used to elevate the official numbers tracking ZEV adoption were down 17.0%. Battery hybrids (HEVs) were largely unchanged with a dip of only 2.3%. From the separate Energy Commission sales data, hydrogen vehicles contributed only 826 to the total true ZEV numbers.

Market share for BEVs was up slightly from the previous quarter at 14.6%. While this number improved, a focus on the market share results shown in the chart above overstates the acceleration in sales of these vehicles. As indicated above, the base used to calculate this metric—the total number of registrations—remains down sharply from pre-pandemic levels. Measured against a more normal level of sales, BEVs instead would come in with a market share in the 11 – 12% range, still an improvement but lower against a broader market with a greater offering of lower price models rather than the current tilt toward higher priced vehicles closer to the BEV range.

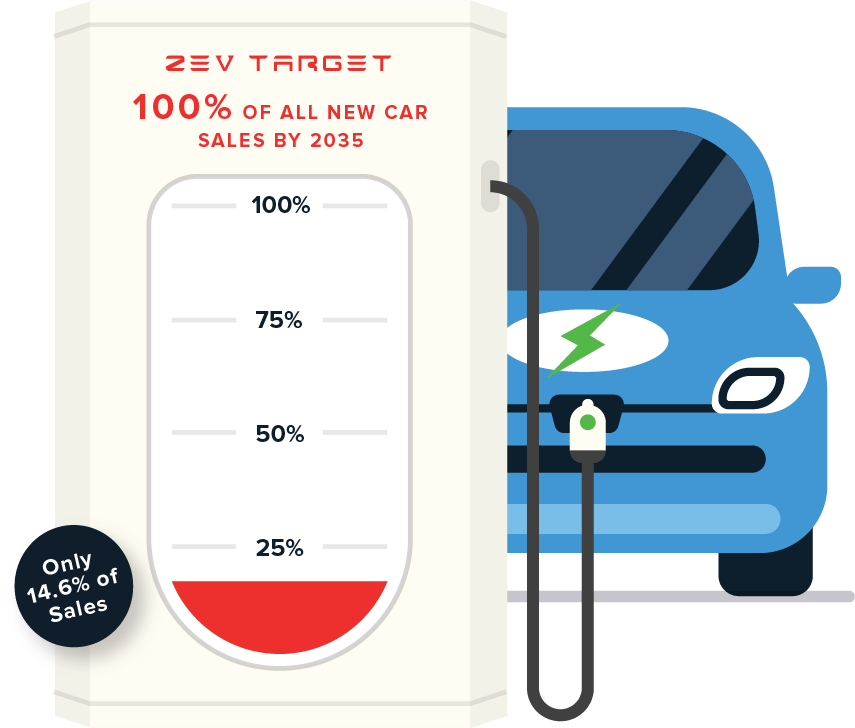

State Goal: 100% ZEVs by 2035

The state previously maintained a goal of 5 million zero-emission vehicles (ZEVs) on California roads by 2030 pursuant to Executive Order B-48-18. Under Executive Order N-79-20, the governor changed this goal to require all new vehicles offered for sale in the state to be ZEVs by 2035 for light duty cars and trucks, and by 2045 for heavy and medium duty vehicles. In spite of the substantial but as-yet unknown costs and other effects of this action including as discussed below the availability of the required battery and related materials, the state agencies are now moving ahead to implement this order administratively using the blanket authorities given to them by the legislature under the climate change program.

California’s sales mandates for ZEVs first began with the Air Board’s adoption of the LEV I regulations in 1990. After four decades, these mandates have resulted in ZEVs comprising 14.6% of new light vehicle registrations in the first quarter of 2022.

Signs of Things to Come?

The 14.6% market share provides an inflated view of ZEV penetration due to the much lower base of total light vehicle registrations. From another perspective, however, the current sales numbers may in fact suggest one possible course for where the market may be heading in response to increasing electric vehicle sales mandates such as California’s pending Advanced Clean Car rule. The current market reflects the convergence of two trends: (1) shift in production to higher margin/higher price vehicles in response to labor and supply chain shortages and (2) shift in demand to higher income households as state actions during the pandemic dampened lower- and middle-income household incomes to a far greater extent.

Reflecting this convergence, the best-selling vehicle in California in the 1st quarter was in fact an electric vehicle, Tesla’s Model Y. Falling in the Luxury Compact SUV class, the Model Y carries a base price of $62,990 to $67,990, or essentially at the Kelley Blue Book average for all new electric vehicles in this period. While federal tax credits can reduce the effective price paid, these credits still are available only to households who can afford to pay $60 thousand or more for a vehicle in the first place. As seen in the federal student loan program’s effect on soaring college costs, subsidies also have the effect of pushing up prices over time.

The recent upward trend in average new vehicle prices stems largely from conditions arising out of the pandemic. At least one major producer, however, has indicated concerns that the accelerated pace for a transition to electric vehicles now being pushed by regulations in areas such as California may prolong these conditions over a much larger term. Recently, Stellantis CEO Carlos Tavares indicated that the accelerated investments required to meet these schedules may be “beyond the limits” of what the industry can maintain:

“What has been decided is to impose on the automotive industry electrification that brings 50% additional costs against a conventional vehicle,” he said.

“There is no way we can transfer 50% of additional costs to the final consumer because most parts of the middle class will not be able to pay.”

Automakers could charge higher prices and sell fewer cars, or accept lower profit margins, Tavares said. Those paths both lead to cutbacks. Union leaders in Europe and North America have warned tens of thousands of jobs could be lost.

In order to avoid this narrowing of the market or at least avoid acknowledging this potential, regulations proposed to accelerate the transition rely heavily on projections that the cost difference between electric vehicles and internal combustion engine (ICE) vehicles will largely equalize by the second half of the decade. Other projections suggest this point may be reached as early as 2024.

These projections, however, are based on historical trends in battery cost reductions that largely were triggered by electric vehicles as a market choice among a range of vehicle types. Electric vehicles had to compete with other fuel types, and competition spurred investment in the cost reductions and new battery chemistries required to bring the price points closer together.

The current regulatory actions such as California’s instead propose leaping ahead to a conclusion that electric vehicles will be the only choice offered to consumers and businesses. And these regulations are coming at a time when: (1) other regulations and policies are pushing for full electrification of broad swathes of the economy and electrification through “clean” but intermittent generation of energy and (2) demand for batteries is also accelerating for a wide range of applications in consumer and industrial products.

As discussed in our report on the 2021:Q4 results, this cumulative demand is putting increasing stress on the supply and consequently the price of the materials essential to this transition. A recent study from International Energy Agency anticipates demand just from their lower range projections consequently will exceed production from both current mining operations and those now under construction by 2028 for lithium and cobalt, and by 2026 for copper. Other assessments expect nickel demand to exceed supply in 2026 as well. Another recent analysis from BloombergNEF expects cumulative demand to exceed known reserves and not just anticipated production supplies for lithium, cobalt, and nickel by 2045 under their Net Zero scenario. Material costs and consequently electric vehicle prices are just as likely to be climbing during California’s anticipated transition period—if available at all—especially when combined with the International Energy Agency analysis showing it takes an average of 16 years to bring new mine capacity on line.

Rather than coming closer together, prices for electric vehicles currently are rising faster. As indicated above, prices for new electric vehicles rose nearly a quarter faster than the average price for all new vehicles over the past year. Taking the two best-selling subcompact models in California in 2021, the Chevrolet Bolt ZEV currently has a base price of $32,000 – $38,000, or double the price of the second-best selling subcompact, the Nissan Versa ICE with a base price of $16,000 – $19,000. Costs may eventually resume converging, but the gap remains large and regulations such as California’s proposal will eliminate the ICE option that is affordable to more of the population at a time of growing material scarcity for what the regulations will allow to remain.

Additional scarcity is likely to occur as producers continue to lock up what supply is available. China, by far the largest electric vehicle market, has secured access to an increasing share of global ore exports and more critically by building 40% – 80% of the total global capacity to process these minerals. Tesla more recently addressed what it has long viewed as a looming nickel shortage by entering into a number of long-term supply contracts, although by necessity these contracts have been for foreign production as the federal government continues to deny permits for major domestic mining projects while apparently slow-walking approvals for others.

As California has pursued its energy policies, the agencies have made constant assurances that the associated costs would be minor. As an increasing series of mandates was placed on the production of fuels, the cost of each new regulation was dismissed as adding only a few more cents to the price per gallon. Californians now pay the highest price for gasoline of any state, currently running 36% higher than the average for all other states and prone to periodic spikes because the state is now regulatorily isolated from the broader national and global fuel markets. The cost of restructuring the state’s electricity generation was also dismissed as minor and at worst absorbable because of our mild climate. The average residential rate is now the highest among the contiguous states, 78% higher than the average paid in all other states, while the average monthly utility bill has gone from one of the lowest in the country to the 21st highest and climbing.

Now in the latest rulemaking, the agencies are giving assurances that a sales mandate on vehicles allowed in the state will have minimal cost impacts—because projections show the price gap should close. The current market conditions should at least be raising questions over the validity of this assumption. The looming supply constraints on critical minerals should be raising even more.

The 1st quarter results shown above indicate there is a significant potential market share for ZEVs, but at the price and supply points arising out of the current pandemic-driven supply and production constraints. These conditions, however, are not dissimilar to ones that could repeat in the future, but this time from a convergence of two different trends: (1) shift in production to higher price vehicles in response to accelerated sales mandates, increased global competition for the critical materials, and the constant risk of supply disruptions from the highly concentrated sources and (2) sustained shift in demand to higher income households as job trends in the state—as contained in the Department of Finance economic projections—driven by current policies continue to see job expansion primarily in high wage and lower-wage industries, with little movement in the middle-class wage gap in between.

Buying for Flexibility

The state agencies, by pursuing a single technology solution to the climate goals, are increasing both the risks and consequences of getting the decisions right, in terms of production availability and costs to consumers and businesses for both new and through the subsequent price effect used vehicle markets. As discussed above, the latest new vehicle results indicate that ZEVs are capable of grabbing a higher market share when that market is pared to its higher-end components, both for demand (income) and supply. Looking at the full California fleet, vehicle buyers when broadened to all income levels instead have taken a more diversified approach.

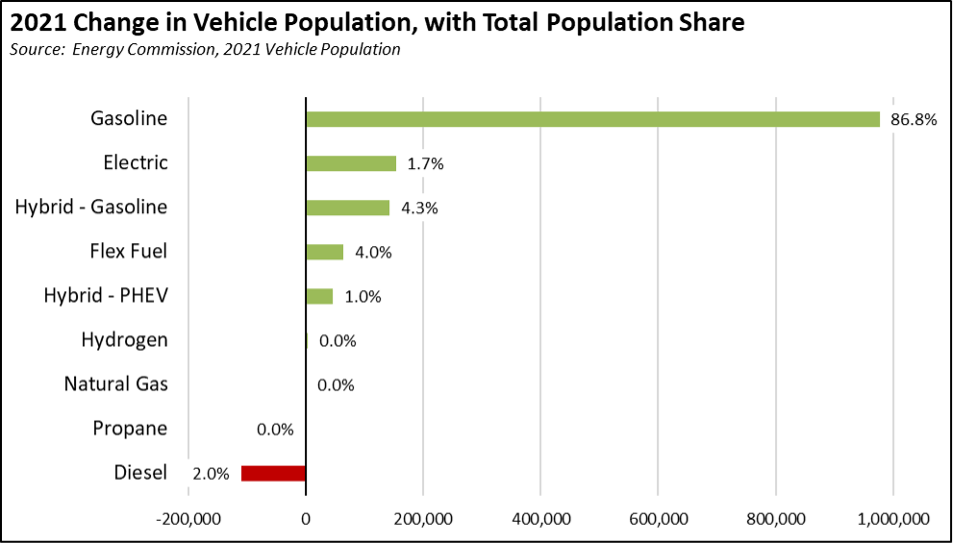

BEVs are a growing presence among total vehicle registrations but still are near the bottom in the range of choices currently available to Californians. In the recently released 2021 vehicle population data from the Energy Commission summarized in the chart below, the number of traditional gasoline vehicles increased more than 6 times faster than electric vehicles (an increase of 977,238 compared to 153,081) in 2021, comprising 86.8% of all registered light-duty vehicles in the state that year.

Considering only the alternative powered vehicles, Californians still showed a defined preference for vehicles that produced greater efficiency and consequently lower emissions, but that also preserved flexibility in responding to shifting fuel markets. Gasoline hybrids (HEVs) alone nearly matched BEVs in growth. Combined, HEVs and the combustion/electric vehicles (PHEVs) formed the next highest vehicle ownership category at 5.3%, followed by flex fuel at 4.0% and even diesel with reduced numbers still at 2.0%. Electric vehicles came at the end of these other categories at only 1.7% of total registered vehicles.

State Energy Transition: Putting the CARB Before the Source

In spite of this continued demonstration that Californians prefer and respond to a range of vehicle offerings, the current policy actions are not only to restrict future options essentially to a single technology but also to begin the closure of current fuel sources even before the attainment of the 100% sales mandate is demonstrated to be feasible.

In addition to 100%, ZEV mandates for light duty vehicles by 2035 and medium- and heavy-duty vehicles by 2045, Executive Order N-79-20 also directed the agencies to “expedite regulatory processes to repurpose and transition upstream and downstream oil production facilities.” In other words, eliminating the fuel source on which 98.1% of current light-duty vehicles in the state depend even before the replacement option coming from the agencies is shown to be feasible or even cost-effective for the full range of California drivers.

State and local actions having the effect of restricting oil and gas production in California already have seen results. In a longer-term view, US Energy Information Administration data shows that total in-state oil production (except federal offshore) went from about 900,000 barrels a day in 1990 to only 354,000 in the latest data from February.

Within the timeframe of the state’s climate change program, Energy Commission data shows that in-state production as a supply source to California refineries dropped 48.2 million barrels (132,000 barrels per day) between 2010 and pre-pandemic 2019.

That drop in in-state production, however, was not matched by drops in in-state use even as the agencies pushed through a cascading series of regulations and public investments in an attempt to shift to electric vehicles, public transit, and “active” transportation modes such as biking and walking. Overall gasoline production increased, growing 3.8% between 2010 and 2019 to fuel both California and neighboring states. Demand for the many other products coming from the state’s refineries continued including materials, fertilizers, chemicals, and other components supporting the production of food and other consumer and industrial products throughout the state.

Reductions of in-state crude production as a source instead were more than matched by increases in imports—a total increase of 69.9 million barrels (192,000 barrels per day) in this period. California’s actions did nothing to reduce emissions from oil use. These actions instead only shifted where those emissions occur and, in the process, shifted where these relatively high-paying jobs are now growing.

These actions likely also increased emissions from the state’s oil use. Aside from the obvious increase coming from the need to transport global sources over longer distances, oil production from the state’s import sources is subject to far less strict controls on emissions of all sorts—air, water, and others—as well as protection from accidents and other discharges. Taking one particular area, the US is the only top oil producer that has reduced flaring associated with production over the past decade.