Below are the monthly updates from the most current November 2022 fuel price data (GasBuddy.com) and September 2022 electricity and natural gas price data (US Energy Information Administration).

Key Takeaways

- The core costs driving California’s energy prices are the state’s regulations and policies. We recently reported these additional regulatory costs estimated at $50 billion annually to households and employers and growing when California prices are compared to the averages in the other states (View in report).

- Regardless of the policy debate, state agencies understand how to reduce these costs. Specifically, testimony presented to the Energy Commission in November indicates that the largest daily gasoline price drop on record came in early October, as a result of Governor Newsom overruling the agencies to allow early production of the lower cost winter formulations to counter the supply shortages that led to price spikes (View in report).

- However, the governor’s proposed oil tax is yet another fuels production tax which continues the policies that have led to the state’s high energy costs and carries the risk of increasing prices even more, both directly from the effects of the tax and from increased risk of supply shortages in the future (View in report).

- If approved, the tax would also increase the costs of all other goods in the state economy due to the reliance on oil to manufacture and deliver essential products to Californians. This proposal would be the fourth major tax increase resulting from legislative action this year, even as the prospects of renewed recession appear to be growing (View in report).

- The proposed tax would in essence act as a price control. As experienced from comparable price controls enacted under President Nixon in the 1970s, price controls limit supply, both directly in immediate markets and longer term by reducing the incentives for capacity investments. They don’t solve a fundamental supply problem. They make it worse (View in report).

- Past investigations into the causes of California’s periodic gasoline price spikes have clearly defined the causes of the state’s periodic fuel shortages and price spikes. Rather than deal with these root causes, the state has consistently ignored the results and imposed more taxes and regulations that lead to more and higher price spikes in the future (View in report).

- Although fuel prices showed sharp drops as refinery capacity and suppliers returned to normal, Californians still paid 48% more than the average in all other states due to the state’s regulations on fuel formulations and production, the highest in the nation fuel taxes, and the state’s general higher operating costs (View in report).

- The average price per gallon of regular gasoline in November was $5.20. Californians are paying $1.69 more per gallon of gasoline than the rest of the US (View in report).

- The more supply constrained diesel prices showed smaller declines. The average price per gallon of diesel in November was $6.15 which means Californians are paying $0.95 more per gallon of diesel than the rest of the US (View in report).

- While gasoline prices are down due to expanding supply and lower costs to produce the winter formulations, other energy costs continue to be pushed higher. California’s residential electricity prices remain the highest among the contiguous US, at 82.4% higher than the average for the rest of the US (View in report).

- For the 12 months ended September 2022, the average annual residential electricity bill was $1,652, 66.2% higher than the comparable bill in 2010- the year AB 32 implementation began. California’s costs went from 9th lowest in the nation to the 18th highest in the latest data (View in report).

- Natural gas prices remained 3rd highest among the contiguous states for commercial rates. California natural gas rates moved up to 4th highest for residential and 2nd highest for industrial rates (View in report).

The Windfall Tax Proposal and the State Economy

The debate over the governor’s proposed oil tax on refineries does not address the much larger costs driving energy prices to these levels as the result of the state’s regulations and policies. We recently estimated these additional regulatory costs at about $50 billion annually to households and employers and growing when California prices are compared to the averages in the other states.

Regardless of the policy debate, state agencies understand how to reduce these costs. Specifically, testimony presented at the Energy Commission’s November 29 workshop indicates that the largest daily gasoline price drop on record came in early October. This steep drop was not the result of state agency actions but the result of Governor Newsom overruling the agencies and allowing early production of the lower cost winter formulations to counter the supply shortages that had led to the price spikes. An unceasing flow of new regulations and taxes has fueled the relentless rise in California energy prices. The only instance of regulatory easing since the state’s current policies began in 2010 is also the only time Californians have seen some relief in this upward climb in costs.

The governor’s proposed tax, however, continues the policies that have led to the state’s high energy costs by adding on to the costs of a product that is already taxed at the highest rates in the nation. If approved, this proposal would also be the fourth major tax increase resulting from legislative action this year even as the prospects of renewed recession appear to be growing.

And by continuing the policy approach that has led to California’s high energy prices, this proposal carries the risk of increasing prices even more, both directly from the effects of the tax and from increased risk of supply shortages in the future:

- The proposal is unlikely to provide significant relief to households and employers. Compliance with California regulations and as critically the effect of those regulations shutting off the state from global supplies produced a cost premium averaging $1.24 higher than the average price in the other states in 2021, a period of reduced demand and prior to this year’s price spikes. The proposed tax would only deal with a small portion of this cost premium, and does nothing to address the much larger price increases coming from the state’s higher fuel taxes, regulatory costs of compliance, and overall higher costs of operating a business.

-

The proposed tax is in essence a price control, and price controls have well defined effects both in the literature and real world experience such as the gasoline price controls enacted under President Nixon in the 1970s. The primary outcome relevant to California’s situation is that price controls limit supply, both directly in immediate markets and longer term by reducing the incentives for capacity investments. In this respect, the proposal is totally at odds with the repeated investigations into the causes of California periodic gasoline price spikes, including investigations as early as 1999, 2000, and 2004 when the cost and supply consequences of the state’s regulations first became apparent. These and subsequent investigations are consistent in three respects: every new price spike leads to yet another round of calls for investigations, those investigations report the same conclusions on why the state’s prices are so high, and those results are ignored and the state imposes more taxes and regulations that lead to more and higher price spikes in the future.

- Supply is the problem. The state’s regulations limit what alternative supplies can be brought into the state even during emergencies. Existing state policies including the proposed tax only serve to make the supply problem worse. The primary factor identified in the previous investigations leading to price volatility is the effect of the regulations limiting supply. The state’s higher taxes and California-specific compliance costs raise the general level of fuel prices overall, but restrictions on supplies that can be sold in the state lead to situations where even minor refinery outages can produce supply shortages and consequent spikes in fuel prices. These supply problems began as the state’s fuel regulations first eliminated the independent refiners who no longer could operate profitably under the growing compliance costs, and have grown as additional refineries have passed this cost threshold. The proposed tax would provide yet another disincentive for capacity investments, adding to but likely accelerating existing state policies implementing the provisions of Executive Order N-79-20 to shut down the remaining refining capacity in the state.

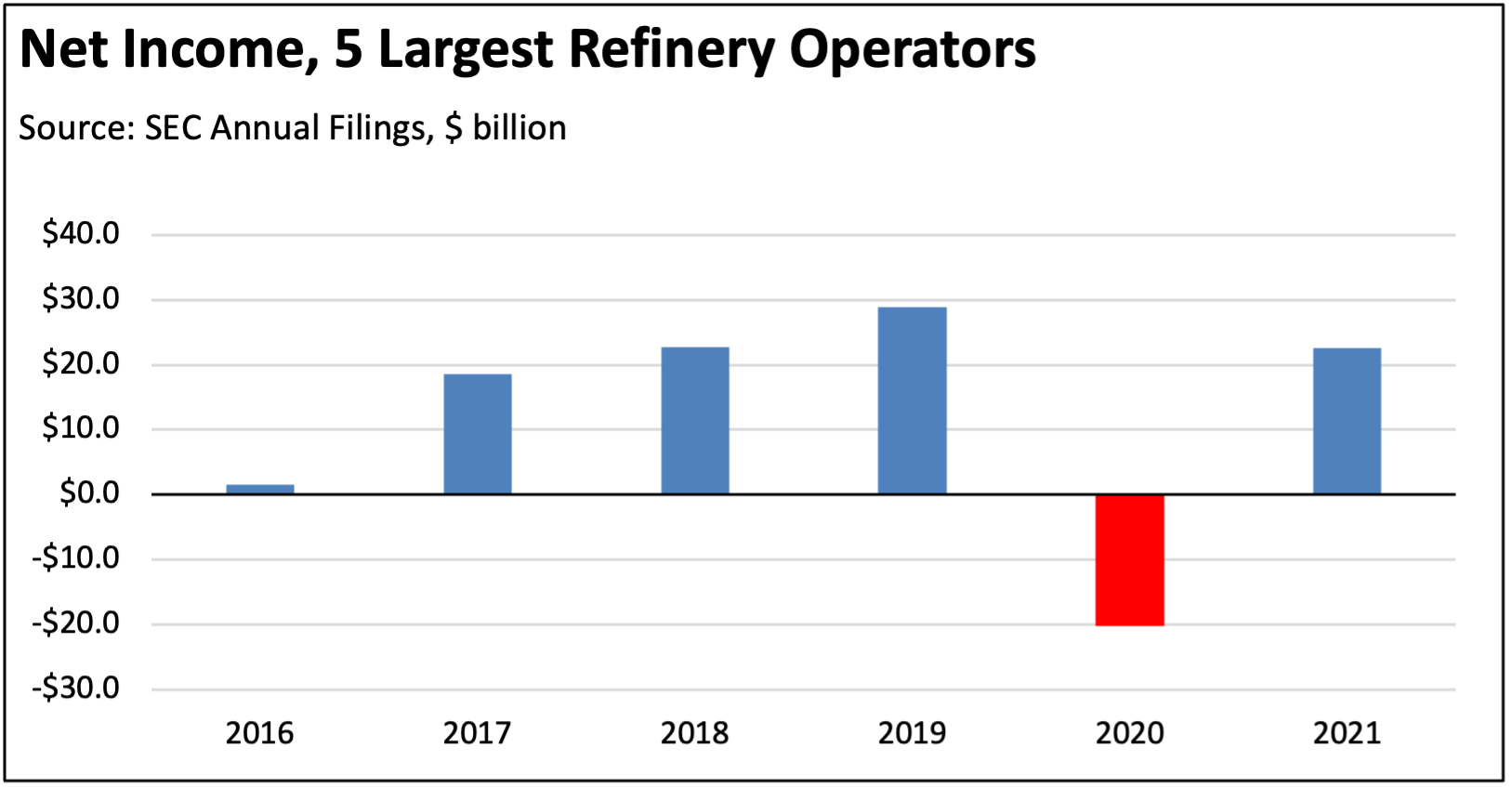

- Given the nature of the agencies involved in the state energy policies, the proposed tax in many respects draws on the pricing model and approach used in state regulation of utilities. These regulations set the rates utilities can charge for their services. The key difference is that existing rate-setting in essence establishes both a minimum and a maximum ensuring the regulated utilities earn an adequate return on their investments and costs. The state retains an interest in ensuring those businesses continue as viable operating entities and that their capital borrowing costs are stabilized through adequate revenue streams. The proposed tax instead serves only to set a maximum price, and ignores the fact that revenues within the oil and gas industry historically are highly variable. For example, SEC filings indicate the net income for the 5 largest refinery operators in California varied widely over the past 6 years, with losses in 2020 nearly matching net gains in 2021. The key difference, unlike the case for other energy providers, is that state policy as contained in Executive Order N-79-20 is to eliminate refineries in the state rather than continue them as viable operating entities. The core consequences will be higher price volatility as an already constrained supply is reduced further.

Inflation Remains at Highest Level Since 1982

California CPI

For the 12 months ending September, the California CPI rose 7.6%, up from 7.5% in August. In the same period, the US CPI rose 8.2%, edging down from 8.3% in August. Looking at the period prior to 2022, California’s rate was again the highest since June 1982.

The Fuel Price Report

Fuel prices experienced a sharp drop as refinery capacity and supplies returned to normal. Monthly average gasoline prices dropped 11.7% in California and 4.2% in the other states. The more supply constrained diesel prices showed smaller declines. This trend has continued, with the most recent CSAA numbers showing regular gasoline down another 9.2% to $4.72 in California on December 6, compared to the US (all states) average of $3.38. California’s average regular gasoline price has dropped to #2 among the states, behind Hawaii. Diesel prices, however, continue at the highest in the US.

Additional price declines are likely in the coming months, but will depend on the extent and whether demand is affected by an increasingly likely economic downturn. Oil prices have been dropping since their near term high in June, and likely will drift down further due to global economic conditions especially softening in China. The wild card continues to be Russian production, including how supply and prices will be affected by current efforts to cap prices for Russian oil.

California vs. US Diesel Price

Above US Average

(CA Average)

The November average price per gallon of diesel in California dropped 32 cents from October to $6.15. The California premium above the average for the US other than California ($5.21) fell to $0.95, an 18.2% difference.

In November, California again had the highest diesel price among the states and DC.

Range Between Highest and Lowest Prices by Region

Above US Average

(Central Coast Region)

The cost premium above the US (other than California) average price for regular gasoline ranged from $1.51 in the Sacramento Region (average November price of $5.03), to $1.96 in Central Coast Region (average November price of $5.48).

Highest/Lowest Fuel Prices By Legislative District:

The asterisks indicate which legislative district races are not yet certified. Final election results will be certified December 16, 2022.

Technical Notes: The electricity data has been updated with the final results for 2021 from Energy Information Administration. In general for California, these revisions produced only marginal change in the residential and commercial rates and about a half percent dip in the industrial rate and average annual residential electric bill. For the states other than California, there was about a half percent dip in all three end user rates and a 1.1% increase in the average annual residential electric bill.

In addition to the monthly electricity data previously available for the US and states, we have added estimates for annual average residential electricity rates at all geographic levels. This new series is discussed in the sections below.

The Electricity Price Report

While gasoline prices are down due to expanding supply and lower costs to produce the winter formulations, other energy costs continue to be pushed higher. Average electricity rates remain the highest among the contiguous states for residential and commercial, and third highest for industrial. Overall, the average household electricity bill soared from 9th lowest among the states in 2010 when the state’s current regulatory drive on energy began, to 18th highest in the latest numbers.

California Residential Electricity Price

Rest of US

California average Residential Price for the 12 months ended September 2022 was 25.74 cents/kWh, 82.4% higher than the US average of 14.11 cents/kWh for all states other than California. California’s residential prices were again the highest among the contiguous states.

California Residential Electric Bill

For the 12 months ended September 2022, the average annual Residential electricity bill in California was $1,652, or 66.2% higher ($658) than the comparable bill in 2010 (the year the AB 32 implementation began with the Early Action items). In this same period, the average US (less CA) electricity bill for all the other states grew only 16.4% ($224).

In 2010, California had the 9th lowest residential electricity bill in the nation. In the latest data, California rose to the 18th highest.

Residential bills, however, vary widely by region, with the estimated annual household usage in the recently released data for 2021 as much as 83% higher in the interior regions compared to the milder climate coastal areas, and substantially higher when comparing across counties.

Applying the 2021 region average electricity rates estimated as below, annual electricity bills vary somewhat more widely, with annual costs up to just over twice as large in the interior compared to the coastal regions.

US Average Price

For the 12 months ended September 2022, California’s higher electricity prices translated into Residential ratepayers paying $10.4 billion more than the average ratepayers elsewhere in the US using the same amount of energy.

Highest/Lowest Estimated Electricity Rates by Legislative District:

Average annual residential electricity rates were estimated by legislative district through the following steps: (1) electric service providers within each district were identified as the primary provider by census tract from the Public Utilities Commission data used in their recent Annual Affordability Report, (2) average annual residential rates by provider were calculated from the US Energy Information Administration annual sales and revenue files, and (3) provider rates were weighted by population using the census block equivalency files for both the new 2022 district boundaries and for the odd-numbered Senate Districts, the 2012 boundaries. The Center’s website also now includes comparable annual rates for counties and California regions estimated using the same method, along with annual rates for states and the US from the EIA data.

As indicated, residential rates vary widely within the state, depending largely on the extent to which providers are publicly owned utilities accessing established hydroelectric sources. All districts, however, are well above the average paid in other states, with state policies pushing the district rates from a quarter higher in the lowest rate Assembly District to 2.3 times as high in the most costly districts.

Estimated 2021 Residential Electricity Rate (cents per kWh)

Source: see text

The asterisks indicate which legislative district races are not yet certified. Final election results will be certified December 16, 2022.

California Commercial Electricity Price

Rest Of US

California average Commercial Price for the 12 months ended September 2022 was 20.97 cents/kWh, 83.6% higher than the US average of 11.42 cents/kWh for all states other than California. California’s commercial prices again were the highest among the contiguous states.

California Industrial Electricity Price

Rest of US

California average Industrial Price for the 12 months ended September 2022 was 16.64 cents/kWh, 114.2% higher than the US average of 7.77 cents/kWh for all states other than California. California’s industrial prices again were the 3rd highest among the contiguous states.

US Average Price

For the 12 months ended September 2022, California’s higher electricity prices translated into Commercial & Industrial ratepayers paying $15.1 billion more than ratepayers elsewhere in the US using the same amount of energy. Compared to the lowest rate states, Commercial & Industrial ratepayers paid $19.7 billion more.

The Natural Gas Price Report

For natural gas, California remains at 3rd highest among the contiguous states for commercial rates, but moved up to 4th highest for residential and 2nd highest for industrial rates.

California Natural Gas Prices

Average prices ($ per thousand cubic feet; 12-month moving average) for the 12 months ended September 2022 and changes from the previous 12-month period for each end user. California remained at 3rd highest among the contiguous states for commercial rates, but moved up to 4th highest for residential and 2nd highest for industrial rates.