Below are the monthly updates from the most current October 2022 fuel price data (GasBuddy.com) and August 2022 electricity and natural gas price data (US Energy Information Administration).

Key Takeaways

- The average price per gallon of regular gasoline in October was $5.90. Californians are paying $2.22 more per gallon of gasoline than the rest of the US. View in report.

- Similarly, the average price per gallon of diesel in October was $6.47 which means Californians are paying $1.31 more per gallon of diesel than the rest of the US. View in report.

- California’s residential electricity prices remain the highest among the contiguous US, at 83% higher than the average for the rest of the US. View in report.

- The core cost drivers behind California’s high energy prices- state regulations and supply vulnerability– remain unaddressed by the state despite numerous past reviews and investigations that came to the same conclusions on these issues.

- The state’s regulations and policies are now costing California households and employers about $50 billion a year more for energy, compared to the average rates in other states, and far more compared to the lowest cost states. View in report.

- Adding to this cost-driver mix, the governor intends to call a Special Session to enact yet another tax on fuels production which, if enacted, would be the 4th major state tax increase this year. View in report.

- The general effects of this tax can be seen in the similar national tax enacted under Jimmy Carter in 1980. This tax was subsequently repealed in 1988 due to a range of negative outcomes, including below-target revenues, increased fuel costs, and discouraged investment in domestic energy production. View in report.

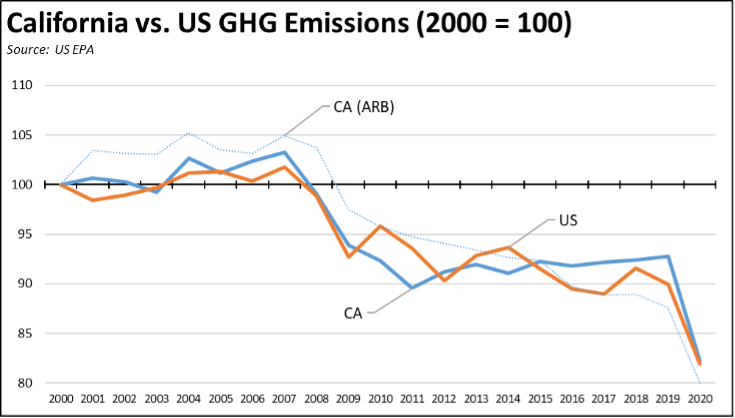

- Most of the state’s GHG emission reductions achieved to date have been associated with economic downturns and restructuring of emission sources- manufacturing out of the state- rather than the state’s climate regulations. While California’s GDP suffered due to the Great Recession, emissions dropped a total of 47.1 MMTCO2e, then another 33.1 MMTCO2e as regulations actually took effect. View in report.

- Emission progress in most years has been outweighed by wildfire emissions, as detailed in a recent report a recent Environmental Pollution report. The 2020 wildfire emissions were substantial, producing an estimated emissions of 127 MMTCO2e, seven times the 2003-2019 average. View in report.

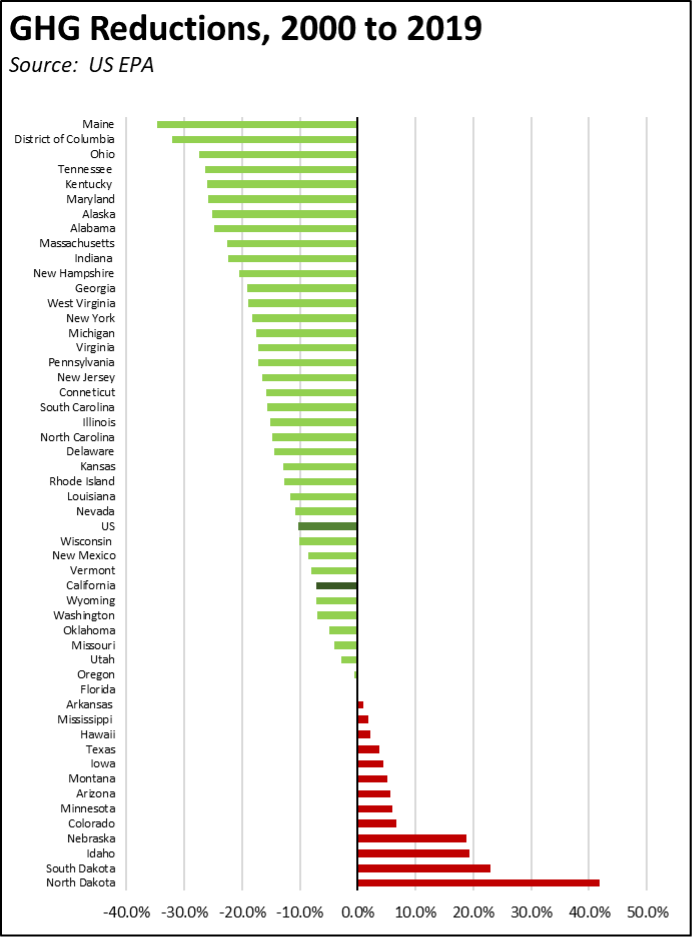

- While California is often cited as a leader on climate change issues, new data from US EPA indicates the regulations behind these costs have put California at only 31st highest among the states and DC when ranked according to the percentage change in greenhouse gas emissions since 2000. View in report.

- In all, 26 states including California were below their 1990 emissions levels in 2019, while the US was close at only 1.8% above. View in report.

The latest results again saw the state’s energy policies in combination with global oil and gas prices pushing California’s energy costs higher in all categories. With alternative supply sources restricted by the state’s regulations, continuing refinery issues saw the monthly gasoline average price rise to $5.90 in October. Prices have since eased as more supply has come back online, with the latest average from CSAA on November 14 down to $5.43 for regular gasoline in California and $3.77 for the US—a 8.5% decline for California compared to a 1.6% dip for the US. Electricity and natural gas rates also continued to climb, with commercial and industrial natural gas rates moving from 4th to 3rd highest among the contiguous states.

The recent rise in gasoline prices has produced yet another round of calls to investigate the causes, continuing the official response that has been issued with some regularity since the cost and supply issues from the state regulations first began to be apparent in 1999, 2000, and 2004. Yet in spite of the reasons behind the sustained cost rise and periodic price spikes in fuel prices being well known, no actions have been taken to deal with the substantive causes stemming from the state’s regulations and tax policies. As a result, the state continues on a regular cycle of price spikes, followed by calls for investigations, followed by price easing as supply conditions return to—at least under California’s regulations—normal trend, followed by inaction on the root causes coming from the regulations and taxes as public and media attention to the issue fades, followed by additional rounds of regulation that drive prices and costs even higher.

Under current state policies, the core causes behind the recent and previous price spikes are on course to become worse. The state’s high fuel taxes are essentially on autopilot to increase in future years. Costs to produce California-compliant fuels will increase as additional formulation changes are implemented along with other regulatory requirements. The current supply vulnerability will increase as the currently-constrained refinery capacity is reduced even further under Executive Order N-79-20.

Further adding to this cost-driver mix, the governor intends to call a Special Session to enact yet another tax on fuel production in the state, in this case a windfall profits tax. This tax if enacted would be the 4th major state tax increase this year even as the risks of renewed recession appear to be rising. In addition to this proposed tax:

- After no action was taken to cancel or delay the annual adjustments, the taxes on gasoline and diesel increased on July 1.

- After only token payments were included in the Budget Bill to reduce the federal Unemployment Insurance Fund debt—including failure to apply federal pandemic assistance funds specifically authorized and used by most other states for this purpose—the payroll tax paid by employers is now on course to rise over the next decade or so, both to retire the federal debt and to continue paying at the highest level of the state tax component.

- With little public awareness, the payroll tax paid by individuals was increased through SB 951 to fund additional benefit payments of $3 billion in 2025, growing to $4.2 billion in 2030.

- Including the state unemployment insurance rate component, these three combined will increase taxes by an estimated $8- 9 billion a year, increasing over time as the fuel taxes continue rising.

While the outcome of this new state tax if enacted will depend on its specifics, the more general effects can be seen in the similar national tax enacted under Jimmy Carter in 1980. That tax was subsequently repealed in 1988 due to a range of negative results: (1) actual tax revenues fell short of projections by 80%; (2) fuel prices continued to increase as the cost of the tax was embedded into costs of production; and (3) the economy become more vulnerable to imported energy and external price determinants as domestic investment was discouraged through this new disincentive.

The proposed tax even if applied in some way to energy rebates will at most cover only a fraction of the sustained cost increases now being driven by state policy and regulations. These costs come from higher prices for fuels, electricity, and natural gas, as well as other core costs of living affected by the climate change regulations such as housing. Compared to the average prices in the other states:

- The additional amount California households and employers paid due to the state’s higher costs of gasoline rose from an estimated $11.7 billion in 2010, to $17.2 billion in 2021. (Based on Department of Tax & Fee Administration net taxable gallon data and GasBuddy.com average prices; 2021 used as the comparison period to net out this year’s price volatility due to global energy prices and refinery issues.)

- The additional amount paid due to the state’s higher costs of electricity rose from $8.9 billion in 2010 to $25.4 billion in the 12 months ending August 2022. (Based on US Energy Information Administration data.)

- The additional amount paid by residential, commercial, and industrial users due to the state’s higher costs for natural gas rose from a $6.6 million savings in 2010 when prices were near the national averages, to $6.2 billion in additional costs in the 12 months ending August 2022. (Based on US Energy Information Administration data.)

In some cases, the regulations driving these higher costs were begun prior to 2010. For example, the renewable portfolio standard for electricity began in 2002, and the state fuel formulation regulations and restrictions began prior to that. But these regulations have been intensified since 2010 as they formed the base of the climate change program, and additional components as currently proposed or being enacted will drive costs even higher. In the case of electricity, the average California residential rate in August already was 80% higher than the average for all other states. Public Utilities Commission data in their recently released Annual Affordability Report indicates rates for the publicly owned utilities alone are now set to spike at least another 20% in the next three years.

In total, the state’s regulations and policies are now costing California households and employers about $50 billion a year more compared to the average rates in other states, and far more when compared to the lowest cost states. The proposed windfall tax will do little to nothing to offset these drivers of the rising costs of living and costs of doing business. The state agencies remain free to increase these costs even further with little oversight or accountability.

These cost impacts vary across the state, with the lower income interior regions more vulnerable to growing costs of energy especially for electricity. In the just released county consumption data for 2021, average household consumption varies as much as 83% between the highest use interior region compared to the lowest use coastal region.

| Region | 2021 Average Household Electricity (kWh) |

|---|---|

| Central Coast | 6,090 |

| Los Angeles | 6,140 |

| Bay Area | 6,310 |

| San Diego/Imperial | 6,700 |

| Orange County | 6,750 |

| Sacramento | 9,400 |

| Upstate California | 9,880 |

| Central Valley | 9,960 |

| Inland Empire | 9,980 |

| Central Sierra | 11,170 |

Source: Energy Commission, Department of Finance Household Estimates

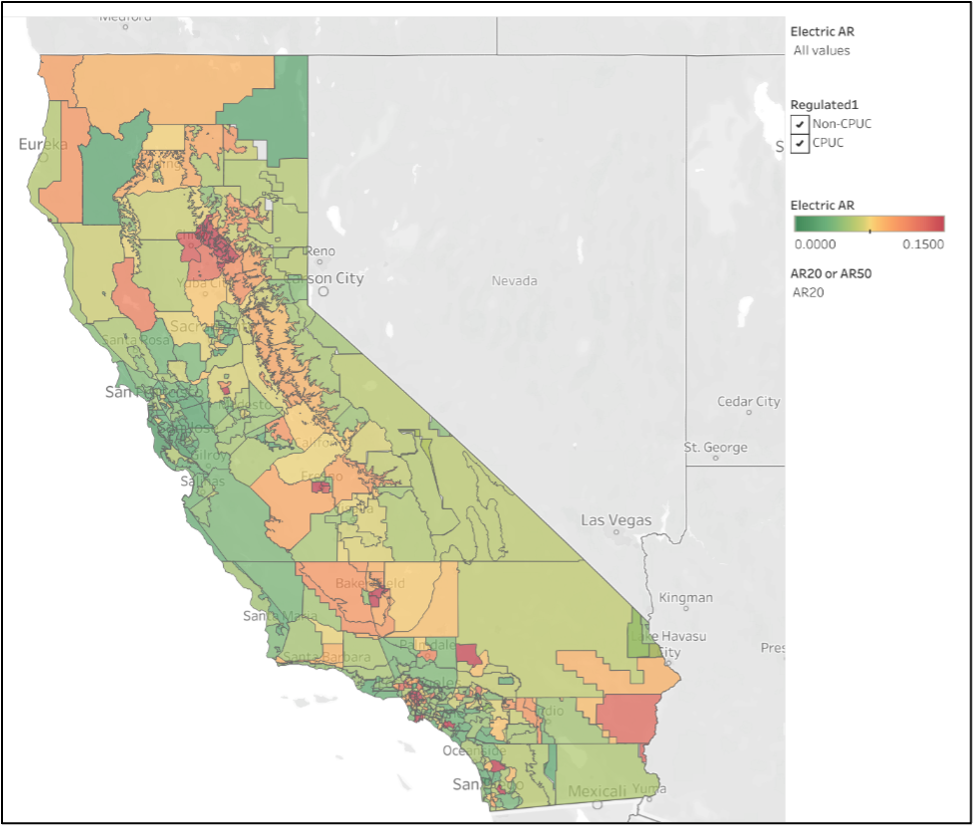

On a more granular level, the just-released Annual Affordability Report from the Public Utilities Commission shows the effect of the state’s high rates on growing energy poverty. In the map below, the Affordability Ratio (AR) is shown for the lowest quintile (lowest 20%) of household income by census tract, calculated as the amount paid for electricity as a share of “discretionary” income (household income less costs of housing and other essential utilities). The areas of concern—those approaching 15% of discretionary income or above for electricity—are concentrated in the Central Valley and lower income portions of the coastal urban areas.

2020 AR20, Electricity, CPUC 2020 Annual Affordability Report

These impacted areas are on track to expand. The 2020 results were moderated to some degree by the income component coming from the high level of federal pandemic assistance that year. As indicated, electricity costs continue to grow, a projected 20% for residential rates in the next three years alone. And as state policies continue to push electrification as the primary solution under the climate change program, these utility costs will make up a rising share of household incomes, not only the bottom quintile but the subsequent tranches as well.

The CPUC report as usual proposes to address these growing impacts through additional subsidies to help cope with the rising costs rather than policy reforms that would solve the problem and reverse this cost trend, much as the proposed windfall profits tax would do in the case of fuels. And in doing so, the report recommendations fail on two primary points. First, this approach at best can soften the cost impacts only to a small portion of households. The far wider effects from the overall cost rises are left in place. Second, this approach adds a self-perpetuating component to the problem. As rates rise, the need for subsidies rises as well. As subsidies increase, rates for the non-subsidized ratepayers will rise even faster to cover those additional costs and push another slice of households into the areas of concern.

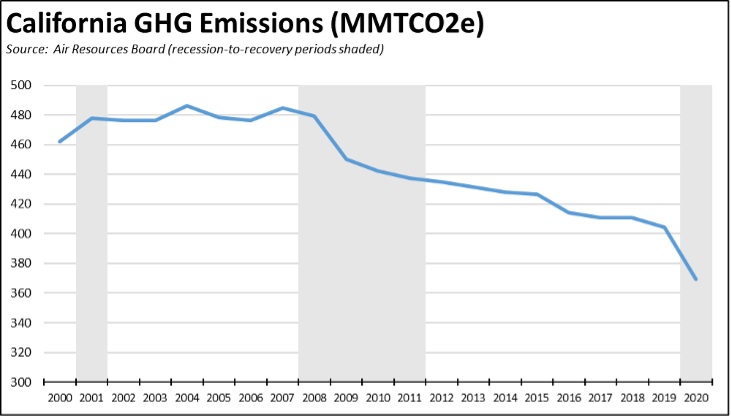

Are these costs justified based on the benefits being achieved? The flip side of the issue is whether Californians are getting something in return for these soaring costs. The recent release of the greenhouse gas inventory update for 2020 provides a basis to evaluate this question. Greenhouse gas (GHG) emissions declined in 2020, but as the accompanying report indicates, these declines were due largely to the state ordered shutdowns associated with the Covid-19 pandemic.

Most of the reductions achieved to date have been associated with economic downturns and restructuring of emission sources such as manufacturing out of the state rather than the state’s climate change regulations. In the Great Recession, California’s real GDP did not recover until the first quarter of 2012. Between the peak in 2007 and 2011, emissions dropped a total of 47.1 MMTCO2e. As regulations then took hold, emissions dropped another 33.1 MMTCO2e through 2019, followed by another 35.3 MMTCO2e in the 2020 downturn. The “de-growth” components since the 2007 peak total 80.2 MMTCO2e vs. the 35.3 MMTCO2e drop during the interim expansion period.

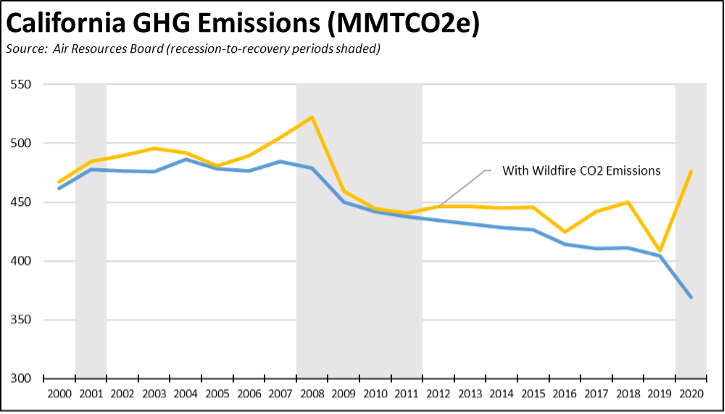

Emission progress in most years has been outweighed by wildfire emissions, as detailed in a recent paper and discussed in various reports. Adding in the Air Board’s wildfire emission estimates to the chart above, the additional costs imposed by the state regulations on households and employers literally have gone up in smoke. In 2020, total emissions incorporating this component in fact rose back to 2008 levels rather than showing a sharp drop. The 2021 wildfire emissions were also substantial, producing an estimated 85.1 MMT of CO2 compared to 106.7 MMT in 2020. While warming has contributed to this source, reductions in forestry and wildlands management on both state and federal lands over the past few decades due to litigation, environmental restrictions, and budgets have been a primary driver as well. Although funding for state activities has increased in the past few years, more cost-effective strategies looking at the total emissions picture still remain.

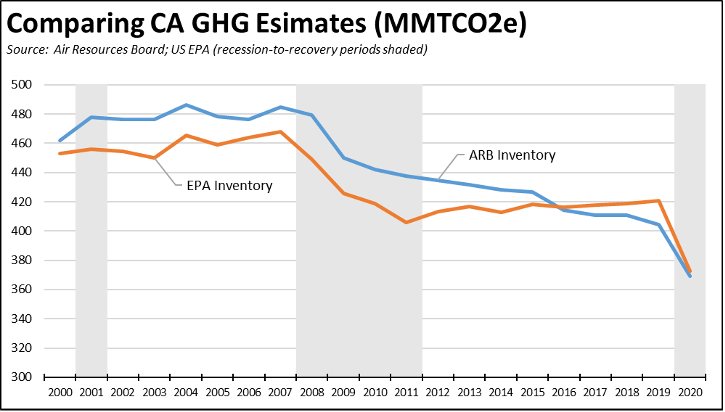

California has often been called a leader in climate change policies, but it has led to pushing out regulations and the cost of those regulations rather than securing emission reductions. US EPA has recently started to include state-level GHG emission estimates in its annual accountings, going beyond the previous estimates by US Energy Information Administration that only calculated state-level COs levels from energy use. In the discussion that follows, these estimates are used rather than the Air Board’s in order to compare California’s emission record with the US and the other states with data using the same methodologies and assumptions.

The EPA numbers differ from the Air Board’s. As shown in the comparison below, the EPA estimates are somewhat lower in the beginning portion of the past two decades, and show a larger drop during the Great Recession. The beginning and end points, however, are close. And though showing some differences in the interim years, the EPA numbers allow a comparison across the states and with the US total using consistent sources and methods that are in compliance with international standards and cover the same anthropogenic sources and sinks and all seven greenhouse gases.

Indexing the estimated emissions to 2000 to provide a comparable metric, there is little difference in the general emissions trend between California and the US. The US numbers show more variation on a year-to-year basis, but the EPA estimates also show little change in California between 2013 and 2019, while US emissions indicate a gradual decline. Even using the Air Board estimates instead (dotted blue line in the chart below), there still is little difference in outcomes between the state and the national numbers. Overall, the key differences lie in the approach, with California promoting a much more intrusive and extensive command-and-control regulatory approach and in the much higher costs coming from that approach.

Using 2019 as the comparison year to net out the pandemic effects, California comes in at the 31st highest among the states and DC when ranked according to the percentage change in emissions since 2000. Even when measured by absolute change in emissions, California still only comes in at 10th best. In all, 26 states including California were below their 1990 emissions levels, while the US was close at only 1.8% above.

Costs are critical, not only to the households and employers that have to pay these soaring bills but also in the future ability of the California measures to make an actual difference to global warming. California’s total emissions in 2019 were only 0.8% of the global total. In its latest October 2021 submittal, China expects its emissions alone to grow between 42 MMT to 1,342 MMT through 2030, or anywhere from 10% to over 3 times as much as California’s total emissions. The growth in China’s emissions is likely to more than overwhelm the reductions California will be able to achieve, even though China has embraced many of the state’s climate strategies and in the process secured near-monopolistic control over many of the battery and new energy materials critical to California’s own success. In its August 2022 submittal, India anticipates its emissions will grow by just over 1,000 MMT in this period. Even former Governor Jerry Brown admitted that California’s program alone will do little to affect global emission levels and will become successful only if its measures are adopted as models by other states and other countries.

The high costs being produced by California’s measures, however, strongly call into question their attractiveness to other states and countries, especially when those costs are measured against its emission achievements to date and measured against what other states have been able to achieve at a far lower cost. Rather than pausing and considering reforms that would meet the climate goals in a more efficient manner, the agencies instead continue on their current course of driving the associated costs even higher, along with the overall costs of living and costs of doing business in this state.

Inflation Running Highest Since 1982

California CPI

For the 12 months ending September, the California CPI rose 7.6%, up from 7.5% in August. In the same period, the US CPI rose 8.2%, edging down from 8.3% in August. Looking at the period prior to 2022, California’s rate was again the highest since June 1982.

California vs. US Diesel Price

Above Average for

Rest of US (CA

Average)

The October average price per gallon of diesel in California rose 16 cents from September to $6.47. The California premium above the average for the US other than California ($5.16) remained at $1.31, a 25.4% difference.

In October, California again had the highest diesel price among the states and DC.

Range Between Highest and Lowest Prices by Region

Average for Rest of US

(Central Coast Region)

The cost premium above the US (other than California) average price for regular gasoline ranged from $2.12 in the Sacramento Region (average October price of $5.79), to $2.41 in Central Coast Region (average October price of $6.08).

Highest/Lowest Fuel Prices By Legislative District

California Residential Electricity Price

Rest of US

California average Residential Price for the 12 months ended August 2022 was 25.37 cents/kWh, 83.2% higher than the US average of 13.85 cents/kWh for all states other than California. California’s residential prices again were the highest among the contiguous states.

California Residential Electric Bill

For the 12 months ended August 2022, the average annual Residential electricity bill in California was $1,616, or 62.6% higher ($622) than the comparable bill in 2010 (the year the AB 32 implementation began with the Early Action items). In this same period, the average US (less CA) electricity bill for all the other states grew only 16.6% ($226).

In 2010, California had the 9th lowest residential electricity bill in the nation. In the latest data, it rose to the 20th highest. Residential bills, however, vary widely by region, with the estimated annual household usage in the recently released data for 2021 as much as 83% higher in the interior regions compared to the milder climate coastal areas, and substantially higher when comparing across counties.

Average for Rest

of US Price

For the 12 months ended August 2022, California’s higher electricity prices translated into Residential ratepayers paying $10.1 billion more than the average ratepayers elsewhere in the US using the same amount of energy. Compared to the lowest rate state, California households paid $13.4 billion more.

California Commercial Electricity Price

Rest Of US

For the 12 months ended August 2022, California’s higher electricity prices translated into Residential ratepayers paying $10.1 billion more than the average ratepayers elsewhere in the US using the same amount of energy. Compared to the lowest rate state, California households paid $13.4 billion more.

California Industrial Electricity Price

Rest of US

California average Industrial Price for the 12 months ended August 2022 was 16.48 cents/kWh, 116.8% higher than the US average of 7.60 cents/kWh for all states other than California. California’s industrial prices again were the 3rd highest among the contiguous states.

Average for Rest

of US Price

For the 12 months that ended August 2022, California’s higher electricity prices translated into Commercial & Industrial ratepayers paying $15.0 billion more than ratepayers elsewhere in the US using the same amount of energy. Compared to the lowest rate states, Commercial & Industrial ratepayers paid $19.2 billion more.

California Natural Gas Prices

Average prices ($ per thousand cubic feet, 12-month moving average) for the 12 months ended August 2022 and changes from the previous 12-month period for each end user. In the revised data for August, California remained the 5th highest among the contiguous states for residential rates but rose to the 3rd highest for commercial and industrial rates.