Highlights for policy makers:

- Economic Trends & the State Budget

- State Budget Still Operating Under Reduced Surplus Rather than Deficit Conditions

- But Final Revenue Outcome Dependent on an Extremely Small Portion of Taxpayers

- And Expenditures will be Affected by Current Reliance on Deficit Spending

- Unemployment Claims Begin to Rise

- CaliFormer Businesses—Another Fortune 1000 Company Moves HQ from California

Economic Trends & the State Budget

Our preliminary review of the jobs and labor data last Friday suggested signs of a general slowing in the state economy:

- Nonfarm wage and salary jobs (seasonally adjusted) grew by only 8,700 in September. The previous two months which in the preliminary results reported a healthy total gain of 45,000 jobs have since been revised to a far more anemic 12,100. Other data indicates jobs performance to date will be revised even lower in the additional adjustments to be released in early 2024. The preliminary benchmark revisions released for March 2023 show total nonfarm jobs 197,800 lower (-1.1%) in California than currently reported, comprising about two-thirds of the total preliminary revisions to the national numbers.

- Over the past 6 months, the separate not seasonally adjusted series shows a total increase of 56,700 nonfarm jobs. Of these, 53% were in very low wage and largely publicly funded Individual & Family Services rather than broader growth in private sector jobs.

- Employment—the number of Californians working—was even more disappointing. Total employment dropped for the third month in a row with a loss of 36,300 and came in at the lowest level since April 2022. The employment numbers have essentially stalled out, and have yet to recover to pre-pandemic levels. While migration of workers to other states contributes to this outcome, the larger problem continues to be the state’s lower labor force participation rate. Simply matching the national average would result in nearly another 100,000 workers in the labor force, pushing the total back to the pre-pandemic peak and providing additional labor supply essential to stronger jobs performance. And given that California, although aging, still has a relatively younger population than the US average, stronger labor force numbers should be possible except for state policies that continue to emphasize benefit payments over actions to expand both the labor supply and the jobs base.

- The state’s economic performance heavily relies on the Bay Area outperforming the rest of the state. With just over 19% of the population, the Bay Area produces over 40% of the state GDP and over 40% of state personal income tax revenues. The job numbers, however, show the Bay Area counties losing 9,600 jobs over the past three months and pushing the total down to just 0.6% above the pre-pandemic peak. The other jobs-critical region—Los Angeles—has shown little change over the past 3 months, and currently is only 0.4% over its pre-pandemic peak. The core engines of the state economy are not giving out signs of a pending take-off, but instead have just barely returned to their previous places on the runway.

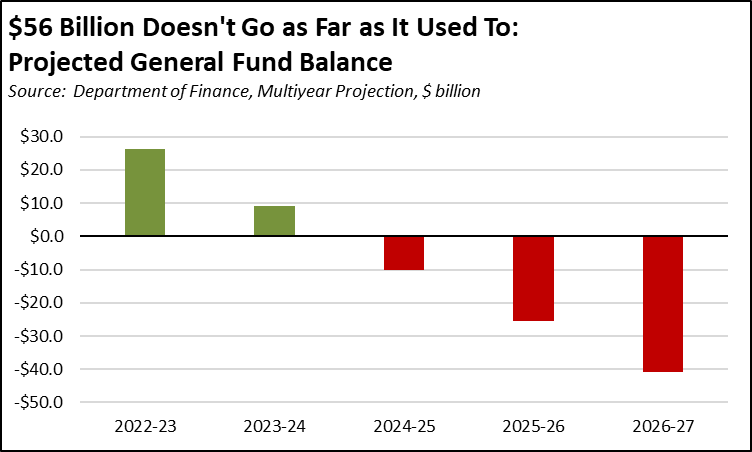

State Budget Still Operating Under Reduced Surplus Rather than Deficit Conditions

A slowing economy has immediate implications to state spending plans, both under the current Budget Bill and projected spending over the 5-year Multi-Year horizon. Anticipated impacts on total revenues, however, will be difficult to project for the upcoming budget cycle that will begin with the Proposed Budget in January. The tax deadline for most counties previously was extended from April to October 16, and recently was extended again to November 16.

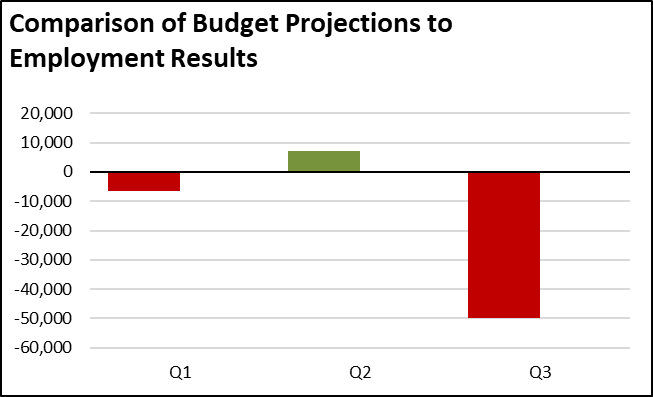

The extent of any downward adjustments in state revenue projections are still uncertain given both the delay in tax collections and the latest economic data. Comparing the latest results to the economic projections underlying the current Budget Bill, the employment results ran close to projections in the first half of 2023, but fell short by 50,000 in Q3. The difference is only 0.3%, but it is a first sign of slowing that would affect revenue expectations as well.

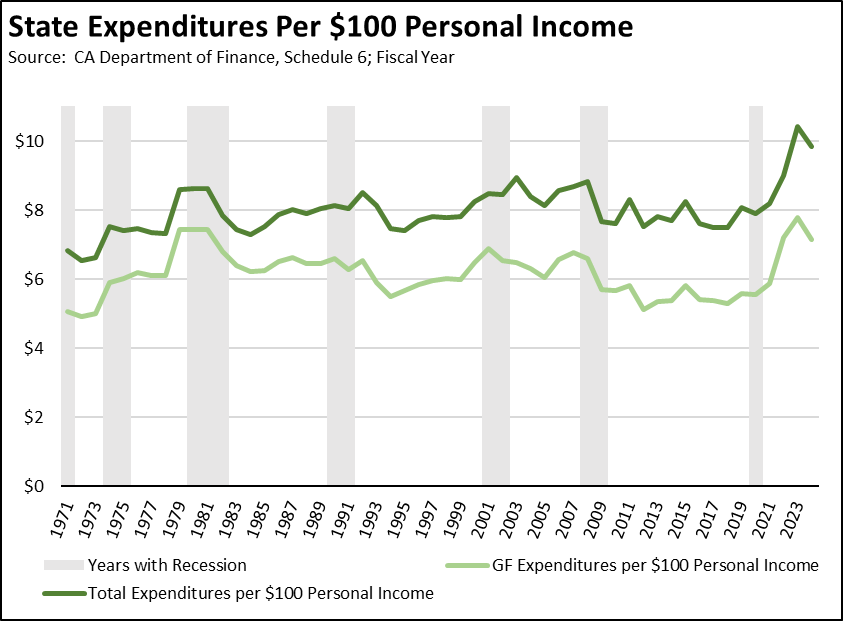

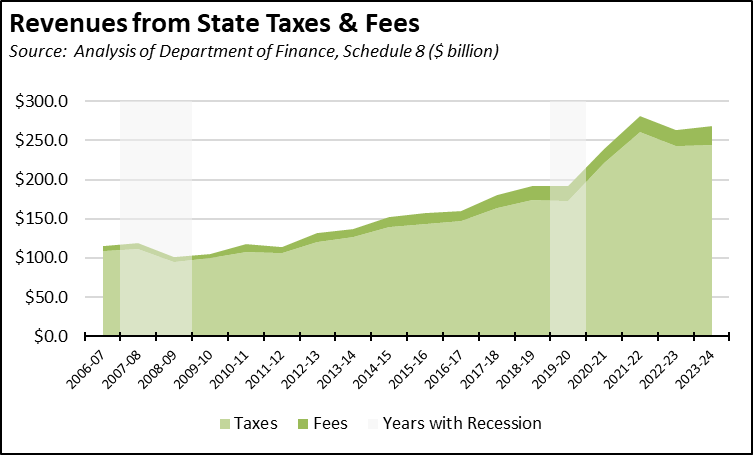

There is, however, plenty of play in the state revenue numbers in particular the portion that truly can be considered “surplus” amounts running above historical levels. Assessing the issue through the spending side, state expenditures as a share of total personal income historically was remarkably stable up until the last few budgets, especially as increasing reliance on fees led to boosts in total expenditures (general, special, and selected bond funds) as taken from the Department of Finance Schedule 6. Revenues and consequently expenditures have been affected by economic downturns in individual years, but the overall level of spending had kept pace with the economy until the upsurge in the last few years.

The surge in expenditures came as revenues pushed into surplus territory in FY 2021 rather than falling into what was otherwise expected to be an historic deficit. From the previous high in 2007-08 to currently projected 2023-24, revenues from state taxes have grown 119%, or at an annual average of 5.0%. Revenues from state fees grew even faster at 252%, or an annual average of 8.2%. In this same period, inflation as measured by CPI-U grew at an average annual rate of only 2.4%.

The numbers in the chart are as of passage of the Budget Bill. The actual results are likely to be higher. The figures for 2023-24 appear to include the SDI tax increase enacted to go into effect this upcoming January. They do not include the additional MCO and guns/ammo taxes separately approved in legislation after the Budget Bill. These two taxes are estimated to yield an additional $1.56 billion annually. Also not included are tax increases related to the ongoing crisis in the unemployment insurance fund as discussed below.

But Final Revenue Outcome Dependent on an Extremely Small Portion of Taxpayers

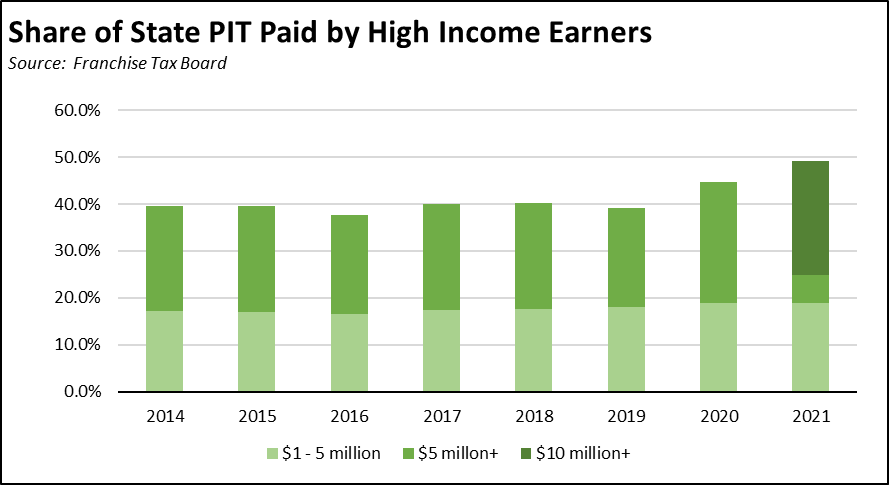

In the current Budget Bill, personal income tax is expected to cover nearly three-fifths of total general fund revenues. Payment of this tax and consequently the overall health of the state budget relies on the economic well-being and residence choice of an extremely small share of the taxpayer base.

In the recently released Tax Year 2021 data from the Franchise Tax Board, high income earners paid 49.2% of all personal income tax (PIT) from resident returns, up from 44.7% from the previous year.

Breaking this number down for 2021:

- Only 0.88% of taxpayers (158,444) with AGI of $1 million or more paid 49.2% of total PIT.

- Of these, only 0.11% of taxpayers (19,471) with AGI of $5 million or more paid 30.4% of total PIT.

- Of these, only 0.05% of taxpayers (8,511) with AGI of $10 million or more paid 24.36% of total PIT.

Note that in 2021, Elon Musk was still a California resident for at least part of the year.

And Expenditures will be Affected by Current Reliance on Deficit Spending

Even with revenues remaining near record levels, the current Budget Bill projects deficit spending in the 5-year Multiyear projections. Rather than increasing reserves in light of the revenue risks from a potential softening in the economic picture, the Budget Bill anticipates using the fund balances built up from the temporary surge in revenues to cover spending in the immediate term. Deficits, however, begin building in 2024-25, further increasing pressures for yet additional taxes and fees beyond those already enacted this year.

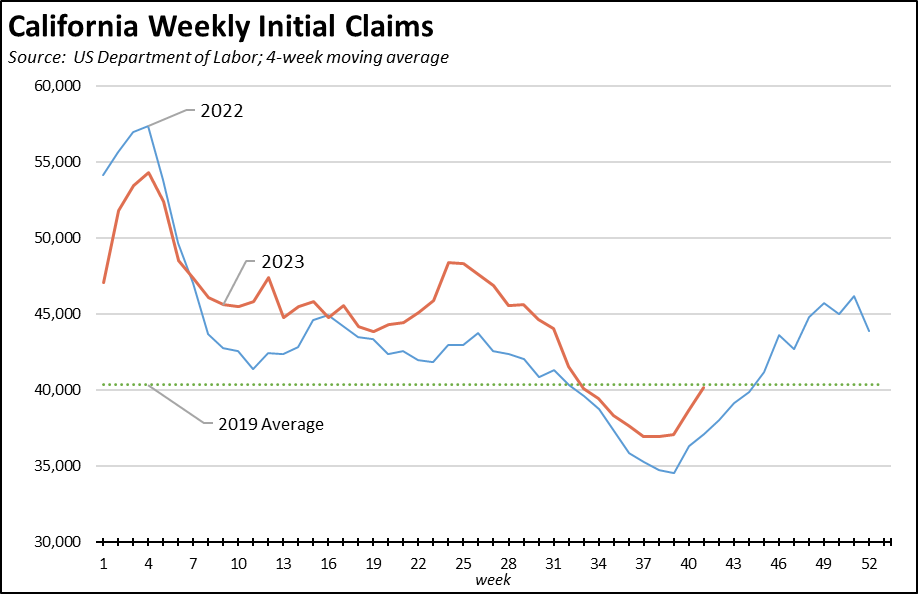

Unemployment Claims Begin to Rise

Initial unemployment insurance claims (4-week moving average) have begun again to rise somewhat above the comparable period in 2022.

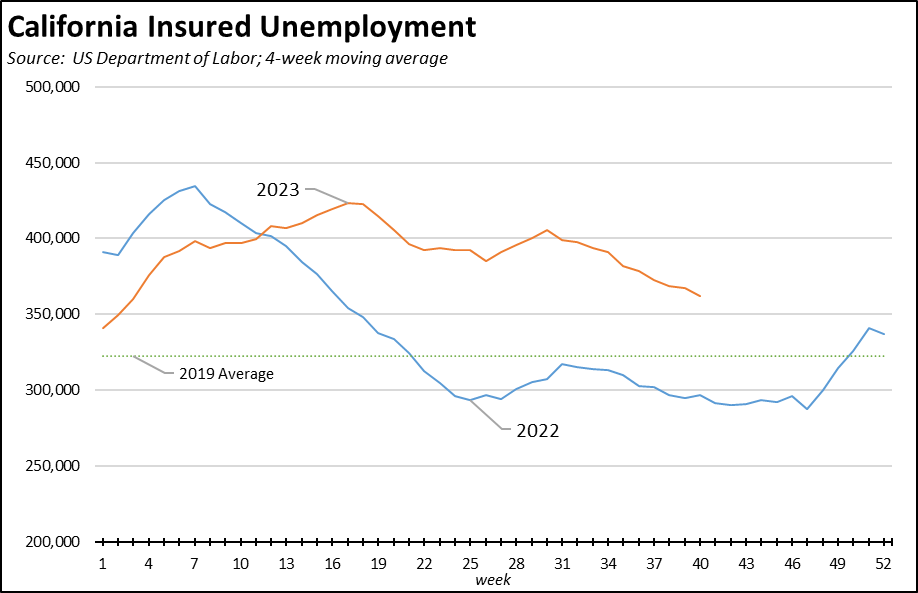

Insured unemployment—a proxy for continuing claims—remained elevated above both the 2022 and 2019 trends, continuing a drag on overall employment and jobs expansion potential.

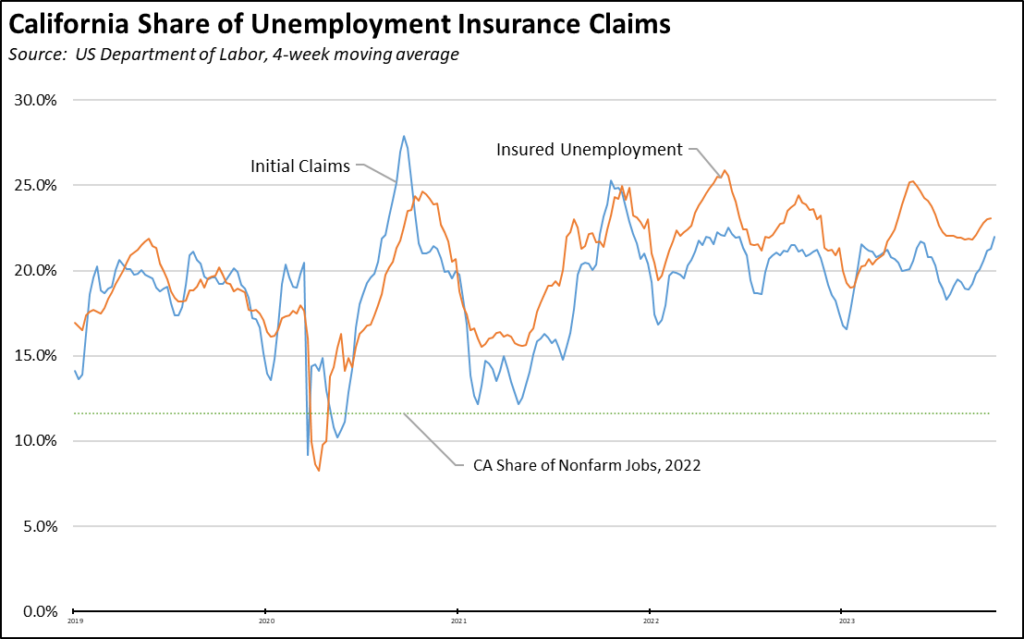

The California program also continues to cover a substantially higher portion of the labor force than in other states. In the latest results (4-week moving averages), California produced 19.5% of all initial claims and 23.1% of insured unemployment. In contrast, California contained only 11.6% of all nonfarm jobs.

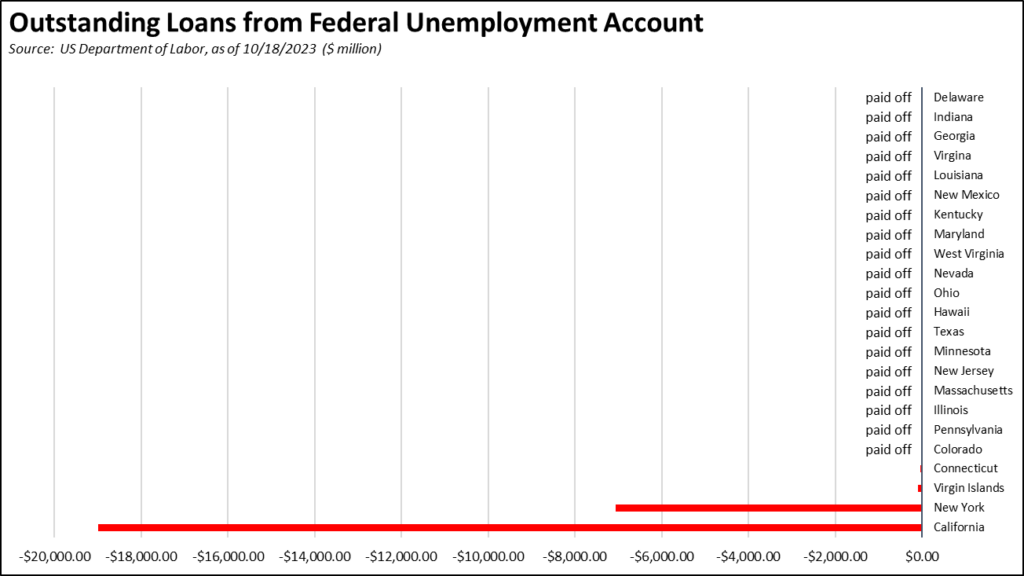

California’s federal unemployment fund debt accounted for 73% of all monies owed by the states, rising to $19.0 billion as of October 18. EDD’s most recent fund forecast projects further deterioration in the fund’s conditions, reaching an expected $20.3 billion deficit by the end of 2024. This fiscal weakening is expected even under a forecast that does not anticipate a new economic downturn in this period.

CaliFormer Businesses—Another Fortune 1000 Company Moves HQ from California

Additional CaliFormer companies identified since our last monthly report are shown below. This month’s entries include another Fortune 1000 company—Advantage Solutions—which recently announced moving its headquarters from California.

The listed companies include those that have announced: (1) moving their headquarters or full operations out of state, (2) moving business units out of state (generally back office operations where the employees do not have to be in a more costly California location to do their jobs), (3) California companies that expanded out of state rather than locate those facilities here, and (4) companies turning to permanent telework options, leaving it to their employees to decide where to work and live. The list is not exhaustive but is drawn from a monthly search of sources in key cities.