Highlights for policy makers:

- COVID-19 and the State Economy

- CaliFormer Businesses: Update

- Employment 993k Below Recovery

- Labor Force Participation Rate

- Nonfarm Jobs: 991k Below Recovery

- Jobs Change by Industry

- Employment Recovery by Region

- Unemployment Rates by Legislative Districts

- Unemployment Rates by Region

- MSAs with the Worst Unemployment Rates

COVID-19 and the State Economy

The overall results from the September numbers show a general slowing of the recovery as another round of local, state, and federal requirements began shifting mask and vaccination enforcement to employers and business operators and as supply chain disruptions continue to reverberate throughout the economy. In the seasonally adjusted series, September’s job increase of 47,400 was still roughly twice the pre-pandemic monthly average of 20,400 in 2019, but was at its lowest level since February this year and was well below the 95,800 gain posted by Texas and 84,500 in Florida. More importantly, with the exception of a few industries, that 47,400 number still largely reflects the reopening of jobs previously closed by the state lockdowns rather than job growth.

The employment increase—the number of people returning to work including through starting a business or other forms of self-employment—of 43,200 was more in line with the numbers seen since April 2021, but still fell short of the 56,900 average in the previous two months. More importantly, 11 states now exceed their pre-pandemic employment levels and moved beyond the recovery stage, while California’s performance to date clocked in at the 8th lowest recovery rate among the states.

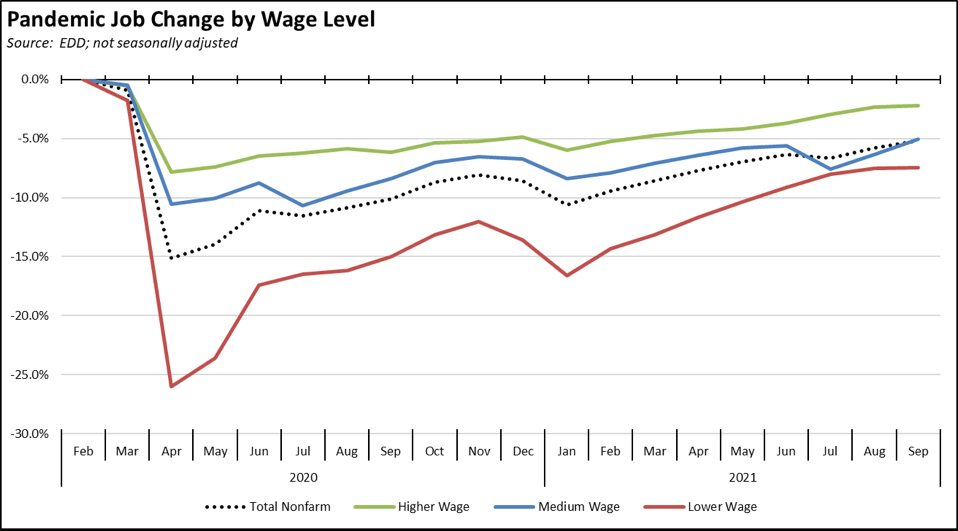

Moving to the more relevant unadjusted numbers, jobs by wage level showed little movement in both the higher and lower wage industries. Gains were highly concentrated (93%) within the medium wage industries, and these in turn were dominated by Government and Educational Services as schools continued to reopen. Jobs within the remaining industries with the exception of Transportation & Warehousing (middle wage) and Administrative & Support & Waste Services (lower wage) were far weaker.

In the chart, higher wage jobs are those industries with average annual wages above $100,000; medium wage is $50,000 to $100,000; and lower wage is below $50,000. Job data is drawn from the industry classifications, unadjusted job numbers, and wage levels generally used in the regular report section below on Nonfarm Jobs.

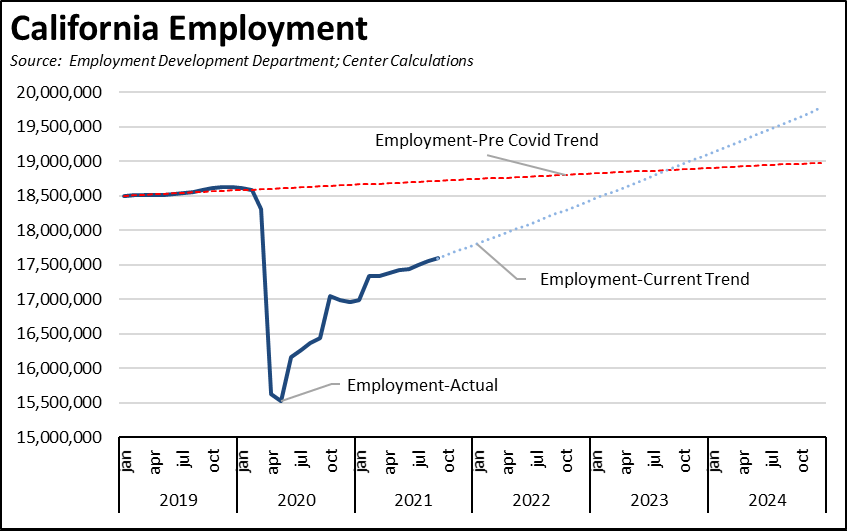

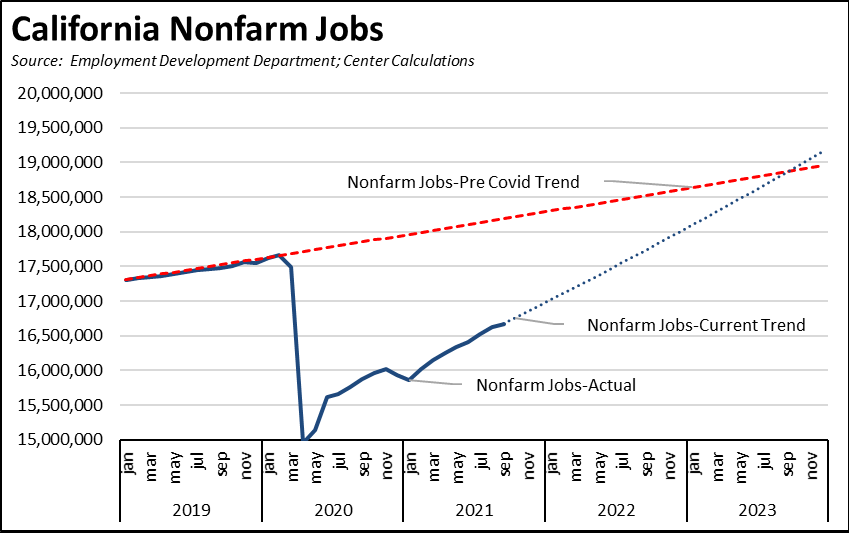

While most of the comparisons in this report and elsewhere measure recovery in terms of the pre-COVID levels in February 2020, the state lockdowns also shut off continued growth that would otherwise have occurred in the previous year and a half. Full recovery consequently should instead be considered by how long it will take for the state to return to trend. Continuing the rates experienced over the past 3 months would return nonfarm jobs and employment to pre-COVID trend levels in mid-2023.

In both charts, the pre-COVID trend is taken from the average monthly growth rate between January 2019 and February 2020. The Current Trend lines are calculated using the numbers from the last 3 months.

The current trend lines in the charts, however, are also facing significant headwinds including notably the escalating supply chain disruptions. These are not just an issue of making sure there are enough televisions on the shelves in time for the holiday sales, but extend throughout the supply chain including increasing shortages of basic goods such as food, parts and components shortages affecting production and production jobs both in the US and overseas, shifting of constrained component supplies production to higher end but higher priced products in order to generate the revenues companies need to survive, and overall inflationary pressures that are now swamping the wage gains lower wage workers in particular have been able to obtain during the current labor shortages. While the federal and state governments have now taken steps to deal with the immediate issues related to port congestion, additional measures will still be required to address the broader factors affecting the breadth of the supply chain.

More broadly, the current situation is also an illustration of the extent to which the current and growing burden of regulations has sapped the amount of resiliency within the state’s economy. Especially for smaller businesses but across most industries, the growing restrictions and costs contained within the state’s high regulation model—including PAGA (Private Attorneys General Act), CEQA, the looming tax increase to pay off the unemployment insurance debt run up by the state during the pandemic, soaring energy costs, the growing costs of housing and commuting for employees, and the full panoply of the state’s approach to regulation—not only increase costs but as well limit the state’s ability to operate in the evolving global economy. Other than the consultants and lawyers that profit off the delays embodied in this structure, the state’s high regulation model does not feed families. Jobs do, and the evolving economy is one where product life cycles are no longer measured in years but in months. In California, that entire cycle can be eaten up by the time required for development and CEQA reviews, regulatory compliance, and bargaining with the many interest groups that use the system to their advantage.

California will still get the knowledge jobs. We still have a competitive advantage here, grounded in no small part by the quality and breadth of the higher education system and the associated research assets. These industries by and large are also little affected by the state’s regulatory structure—one of the core reasons they have been able to prosper to the outsized extent they have while other parts of the state have lagged or experienced more moderate growth.

We also will still get the population serving and tourism related service jobs. These have far fewer location alternatives and have to be here, but they have lower wage structures and often have high seasonal fluctuations. They are more affected by the state’s regulatory restrictions, but instead have to pass these costs on in pricing that adds to the growing costs of living in our state. These two components in essence comprise the structure of how the state’s economy has grown since the Great Recession.

The traditional middle class job base has seen the greatest effects, as illustrated by the state’s efforts to promote an electric vehicle industry as the cornerstone of its green/clean energy jobs strategies over recent years. Electric vehicles (EVs) in essence can be considered a bellwether industry for the state and its efforts to replace the existing jobs base with those fitting a “build back better” or “high road jobs” rubric. The modern electric vehicle industry was created by and in California, beginning with its first requirements under the LEV I regulations in 1990. Subsequently as the regulations evolved to become more proscriptive, expanding electric vehicle and component manufacturing within the state became a central goal of the state’s climate change policies and its professed commitment to creating green and clean energy jobs as an alternative to the traditional middle class jobs being hamstrung by those policies.

The outcome of that goal, though, has remained largely limited to Tesla, which chose to open here because California still had one remaining vacant vehicle production facility in Fremont that could be repurposed quickly and with few regulatory delays. The possibility of expanding jobs at that plant even remains as indicated by the company in their recent announcement of their headquarters move to Texas.

But we are not getting the new plants. Tesla is building new gigafactories in Texas, China, and Germany, with Austin nearing operation just over a year from when it was announced—comparable to the schedule the company was able to follow for its battery gigafactory in Nevada. In recent announcements, Volcon, REE Automotive, and other startups are moving to the industry cluster now developing around Tesla in Texas. Lucid, ElectraMechnicca, and other startups are creating a second production cluster in Arizona, in proximity to their California knowledge components but without California taxes and regulations. Recent announcements by Ford, GM, Volkswagen, and Mullen indicate the traditional US automakers are increasingly concentrating their EV production in Tennessee due to its low electricity costs and taxes, development process, and right-to-work policies, while Ford earlier announced it was building its new Mustang Mach-E SUV in Mexico in order to cut costs and produce the vehicle at a more competitive price point. Globally, actual government support beyond policy statements has seen China leap ahead as the center of the EV industry, with more than 400 domestic companies and most global producers active in the production chain.

Electric vehicles briefly became California’s number one export product in 2020, but only if the ranking is done using the most detailed six digit product coding that compares sales from an industry that exports essentially one product at this level—electric vehicles—to industries that export under multiple product codes. For example at the six digit level, almond, walnut, and pistachio exports cover 6 different product codes, with separate entries for each nut and for shelled and unshelled versions. Combining just these 6 and still ignoring other tree nut products and products that use California grown nuts as an ingredient supporting other California jobs surpasses the electric vehicle export value by 25% in 2020. Similarly, just looking at crude and refined petroleum products puts exports of this industry component at 3rd in 2018 and 2019 and still 9th in 2020 despite the sharp drop that year in oil prices, and these rankings still do not include exports of chemicals, fertilizer, plastics, fibers, solvents, adhesives, and the other nearly 6,000 products dependent on this industry including many that are still produced in California with California jobs as the result of that industry being located in the state. The ranking depends on how the ranking is done.

More critically from a jobs perspective and as an evaluation of the state’s policies, this outcome occurred because Tesla’s sales essentially stalled in the US as fewer EVs overall were sold in California and the US than expected. The company instead turned to exports to Europe to maintain its sales growth. Using the detailed product codes, California EV exports ranked 8th in 2018 ($3.0 billion), 2nd in 2019 ($7.2 billion) as Tesla shifted to European sales, 1st in 2020 ($5.7 billion) as other exports sharply declined during the pandemic, and 2nd ($4.6 billion on an annualized basis) in the year-to-date results for 2021. Beyond the obvious effects of the pandemic period on overall trade levels, exports for California production of this product are likely to decline further as the primary state producer completes opening of production in the export markets (China and EU). California has failed to secure the production of EVs envisioned in its climate change and green/clean energy goals that would lead to a long-term export presence. Instead, the 2020 ranking reflects more a transitory achievement while the company and the industry worked to establish those jobs and that export capacity in other locations.

California’s lead in actual green/clean energy jobs is lagging in other areas as well. US Energy Information Administration data indicates California currently has 8.2 GW of planned new solar capacity, accounting for 17% of the US total but ranking 2nd behind Texas at 12.0 GW. In wind, California ranks 19th with only 0.3 GW in planned new capacity, while Texas leads with 7.6 GW. Even while the state promotes clean energy in its policies, constructing these projects is easier elsewhere.

California has created green/clean energy jobs, but not at the 500,000 level cited repeatedly since at least 2007 with little change by the proponents. Only a portion of these have been permanent jobs, with the number instead relying on temporary construction and installation jobs dealing with equipment produced elsewhere, including solar panels (67% of global shipments from China; 1% from US), lithium-ion batteries (China with 80% of raw material refining and 77% of cell capacity), and wind turbines built in other states and countries.

Even accepting the latest iteration of the 500,000 standard—485,000—at face value, clean energy jobs would account for only 3% of total nonfarm jobs in the state. In another context, this number is only equivalent to 16% of the jobs that were lost due to the initial round of the state lockdowns last year. Even after 3 decades of the state trying to jump start an EV industry and more than a decade of the state’s climate change program, green/clean energy jobs still have to reach a level where they present a real wage and income alternative to traditional middle class jobs.

Green/clean energy jobs as a goal, however, has remained just that. Beyond subsidies to higher income households to promote purchases of products steadily being produced in other states and countries, the state has done little to actually promote creation of these jobs within the state. Energy costs continue to rise towards the highest in the nation. Employment law has become more punitive. Taxes and fees continue to increase. Schools have produced only a portion of the requisite skills even as their funding continues to rise. The reasons for delays and higher costs under CEQA continue to expand. Worker housing has become more costly and scarce, while the commutes on which these workers rely have become longer and divert a greater share of their earnings and time.

The failure of the state to capitalize on the EV industry it created is illustrative of the broader challenges facing the state and its inability to maintain a healthy middle class jobs base as a bridge to upward economic mobility. California has experienced astounding economic success through its tech and other knowledge-based industries—jobs that boomed without state promotion and largely without state interference through regulation. But these are higher-wage jobs requiring a higher level of skills, and these skills increasingly are taught by the public schools to only a share of the students, meaning many of these jobs are filled not by Californians but by workers here on temporary visas. The middle class job base that once provided the foundation for the California dream and the ladder for millions to upward economic mobility has been eroding under the weight of the state’s high tax and high regulation model. The only answer the state has provided is goals without action, and consequently promises without jobs.

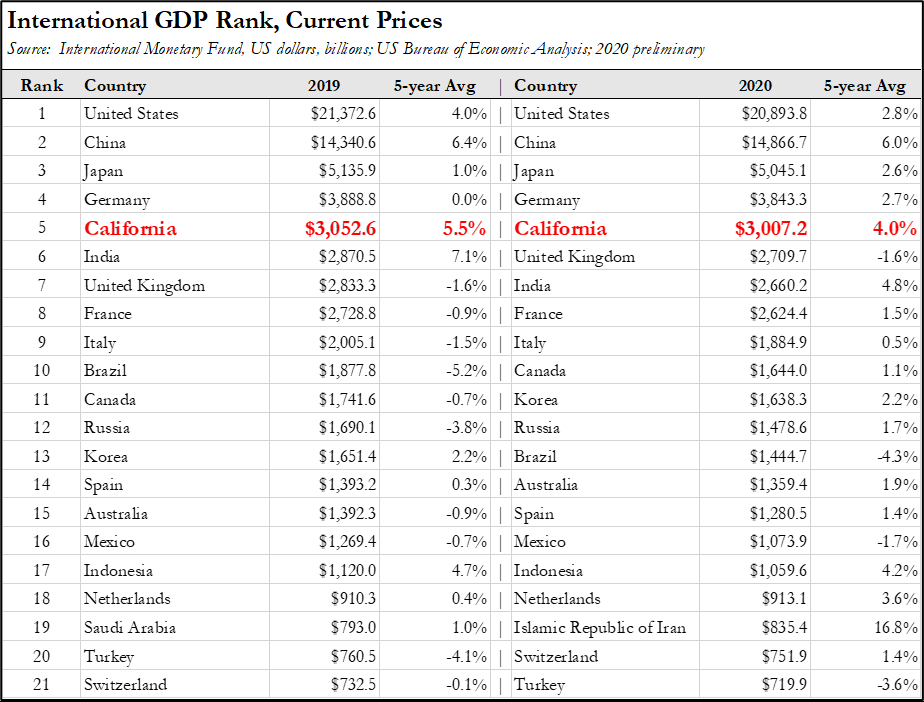

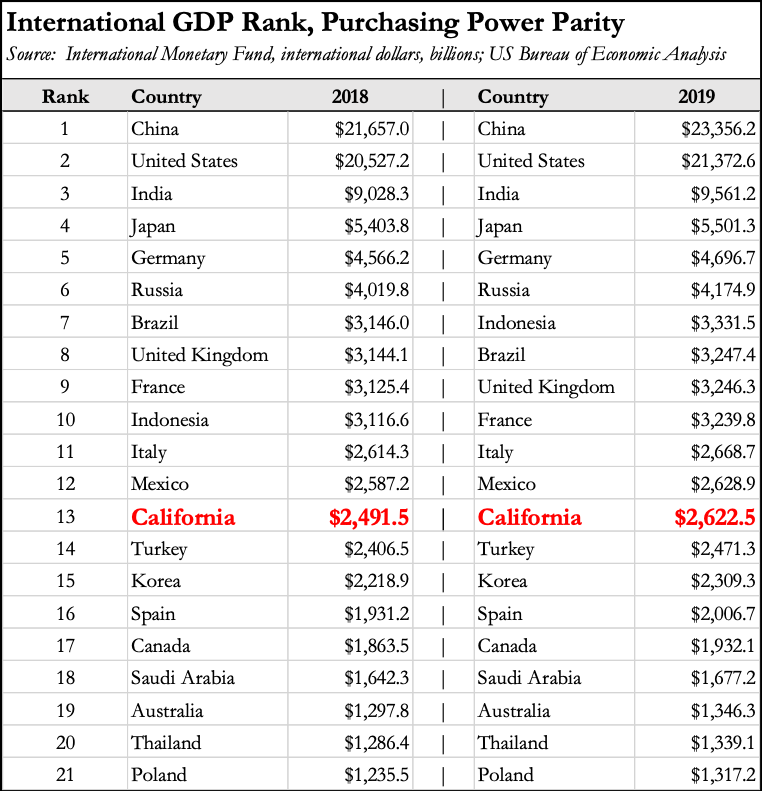

California’s International GDP Ranking Falls to 13 When Adjusted for Cost of Living & Doing Business

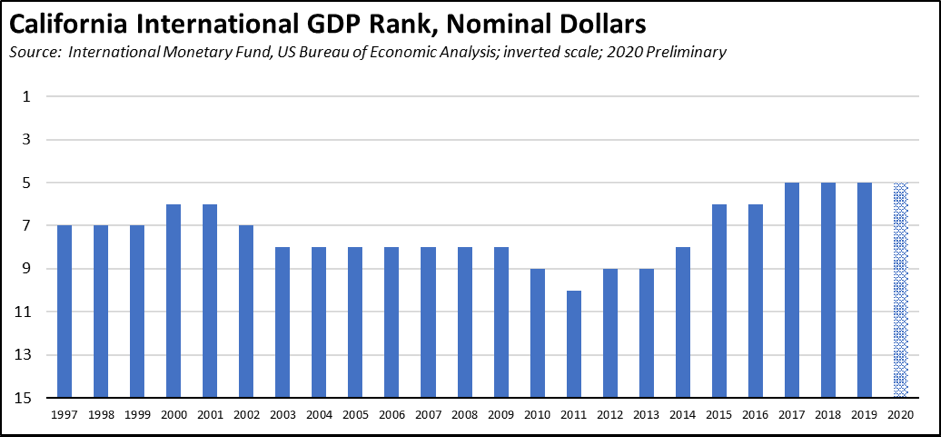

Measured in nominal dollar terms, California’s economy again ranked as the 5th largest in the world in 2019. On a preliminary basis, California appears to be ranked 5th in 2020 as well, although complete data for all countries in the top 20 is not yet available.

The full measure of an economy, however, is not just the size of its GDP, but also the goods and services available to the people within it. While California has steadily moved up the ranks since 2011 in nominal terms, state policies have acted to dissipate much of that growth through continuously rising costs of living. This situation is fully illustrated by the number of tech industry workers in the Bay Area who while making six-figure incomes, still struggle with the high costs of housing, commuting, taxes and fees, and everyday expenses. This burden is magnified throughout the state and felt even more keenly by households faced with the same high cost structure but without the same level of income.

Adjusting for comparative costs, California ranks substantially lower, falling just below Mexico as the 13th largest economy. State policies driving up costs of living in fact have largely offset GDP growth and kept California in this position since at least 2008.

Originally, the notion of ranking California’s economy against other nations was reported in data maintained by Department of Finance. The data sources used in various years, however, have not been consistent and do not appear to have been updated as the underlying data has been revised.

In the analysis presented here, data for the rankings comes from the most recent sources used in the Finance indicator. National GDP is from International Monetary Fund’s World Outlook Economic Database, updated each April and September/October just prior to the IMF meetings. Data for California is from US Bureau of Economic Analysis as recently revised.

Using consistent sources, California’s rank previously hit a high as the 6th largest economy before falling after the Dot.Com Crash and subsequent electricity crisis at the beginning of the 2000s. The state then reached a low of 10th largest during the Great Recession, but subsequently rose to 5th largest following the quick recovery and outsized growth coming from the Bay Area.

Based on the 2019 rankings, India previously was on course to bypass California within 5 years. Economic disruption coming from the various responses from the pandemic now make this outcome more uncertain. Continued growth within the Bay Area in the pandemic period while other parts of the state and globe have fallen behind likely mean that California’s position will be maintained at least for a few years longer.

But these rankings are only from the nominal results. Adjusting to reflect differences in costs indicates the full scale of California’s current and ongoing cost of living crisis.

IMF also maintains a data series incorporating these comparative costs. Nominal GDP is adjusted to international dollars, calculated as purchasing power parity to the US dollar.

Data in the following table is consequently taken directly from the IMF numbers for the listed countries. The California entry again uses the Bureau of Economic Analysis data, but adjusts these numbers using the Bureau’s Regional Price Parity (RPP) series to calculate an equivalent purchasing power parity against the national total. RPP is currently available 2008 through 2019, but the results for 2020 will be provided once the updates and revisions are published in early December. While the results for 2019 are just short of a tie for 12th place with Mexico, the results indicate California has remained in 13th place throughout the period the RPP data is available.

Statements regarding California’s status as the 5th largest economy are often accompanied by the contention that this outcome is evidence that high regulation and high taxes do not harm economic growth. Putting the data into purchasing power equivalency instead reinforces the fact that policy choices have consequences, in this case with the price paid by the households and employers facing an unceasing rise in basic costs.

CaliFormer Businesses: Update

Additional CaliFormer companies identified since our last monthly report are as follows. These companies include those that have announced: (1) moving their headquarters or full operations out of state, (2) moving business units out of state (generally back office operations where the employees do not have to be in a more costly California location to do their jobs), (3) California companies that expanded out of state, and (4) companies turning to permanent telework options, leaving it to their employees to decide where to work and live.

| wdt_ID | Companies | From | To | Reason | Source | Year |

|---|---|---|---|---|---|---|

| 167 | 1Life Healthcare Inc. | San Francisco | Atlanta | Expansions | Read More | 2021 |

| 168 | Aatonomy | San Francisco | Houston | HQ move | Read More | 2018 |

| 169 | Abyss Creations | San Marcos | Las Vegas | HQ move | Read More | 2021 |

| 170 | Adlucent | Irvine | Austin | HQ move | Read More | 2019 |

| 171 | AFC Finishing Systems | Oroville | Idaho | HQ move | Read More | 2020 |

| 172 | AgencyKPI Inc. | Los Angeles | Austin | HQ move | Read More | 2020 |

| 173 | Aging 2.0 | San Francisco | Louisville | HQ move | Read More | 2020 |

| 174 | Airbrake Technologies | San Francisco | Austin | HQ move | Read More | 2020 |

| 175 | Alfresco Software Inc. | San Mateo | Massachusetts | HQ move | Read More | 2019 |

| 176 | Alpha Paw LLC | San Francisco | Austin | HQ move | Read More | 2021 |

| 177 | Alpine Technologies | Torrance | Michigan | HQ/manufacturing move | Read More | 2019 |

| 178 | Alto Pharmacy | San Francisco | Denver | HQ2 | Read More | 2018 |

| 179 | Andamiro USA Corp | Gardena | Texas | HQ move | Read More | 2021 |

| 180 | Anpac Bio | San Jose | Philadelphia | HQ move | Read More | 2019 |

| 181 | Aqua Metals Inc. | Alameda | Reno | HQ/manufacturing move | Read More | 2018 |

| 182 | Arcturus Aerospace | Oxnard | Arkansas | HQ/manufacturing move | Read More | 2020 |

| 183 | AtScale | San Mateo | Boston | HQ move | Read More | 2019 |

| 184 | Aviat Networks Inc. | Milpitas | Austin | HQ move | Read More | 2019 |

| 185 | Axiom Memory Solutions, Inc. | Irvine | Austin | HQ move | Read More | 2019 |

| 186 | Battle Motors Inc. | Venice | Ohio | EV truck manufacturing | Read More | 2021 |

| 187 | Bedrock Sandals | Richmond | Montana | HQ move | Read More | 2019 |

| 188 | BH North America | Los Angeles | Los Angeles | HQ move | Read More | 2018 |

| 189 | Callaway | Carlsbad | Salt Lake City | HQ move | Read More | 2020 |

| 190 | Canoo Inc. | Torrance | Texas, Oklahoma | EV manufacturing and HQ move | Read More | 2021 |

| 191 | Cicero Institute | San Francisco | Austin | HQ move | Read More | 2020 |

| 192 | Clean-Energy Corp. | Newport Beach | Texas | $1 billion solar power/battery manufacturing | Read More | 2021 |

| 193 | CodeBoxx | Sausalito | Florida | HQ move | Read More | 2021 |

| 194 | Cognito | Palo Alto | Oregon | HQ move | Read More | 2021 |

| 195 | Conner Logistics | Fresno | Kentucky | HQ move | Read More | 2021 |

| 196 | Crossfit LLC | Scotts Valley | Colorado | HQ move | Read More | 2020 |

| 197 | Daily Wire | Los Angeles | Nashville | HQ move | Read More | 2020 |

| 198 | DIQ SEO | Silicon Valley | Texas | HQ move | Read More | 2021 |

| 199 | DMG | Newport Beach | Ohio | HQ move | Read More | 2021 |

| 200 | EnerBlu Inc. | Riverside | Kentucky | HQ move | Read More | 2018 |

| 201 | Fantic USA | Sausalito | Denver | HQ move | Read More | 2019 |

| 202 | Flatirons Solutions | Irvine | Colorado | HQ move | Read More | 2018 |

| 203 | Fox Factory | Scotts Valley | Georgia | HQ/manufacturing move | Read More | 2018 |

| 204 | Ganymede Games | Alameda | New Mexico | HQ move | Read More | 2019 |

| 205 | GetSales | San Francisco | Austin | HQ move | Read More | 2018 |

| 206 | Gilad & Gilad | Los Angeles | Texas | HQ move | Read More | 2018 |

| 207 | Glock Store | San Diego | Nashville | HQ move | Read More | 2018 |

| 208 | Grinds LLC | Oakland | Indiana | HQ/manufacturing move | Read More | 2019 |

| 209 | GrowthPlug | San Jose | Oregon | HQ move | Read More | 2019 |

| 210 | GuineaDad | Los Angeles | North Las Vegas | HQ move | Read More | 2020 |

| 211 | H.E.R.O.S. Inc. | Santa Clarita | Arizona | HQ move | Read More | 2019 |

| 212 | Hall Technologies | Tustin | Texas | HQ and manufacturing move | Read More | 2021 |

| 213 | Haptx / Axon VR | San Luis Obispo | Washington | HQ move | Read More | 2021 |

| 214 | Honor Home Care (HQ2) | Concord | Austin | Second operations center | Read More | 2018 |

| 215 | Iron Ox | San Carlos | Texas | Second expansion | Read More | 2021 |

| 216 | IT Avalon | Brentwood | Reno | HQ move | Read More | 2021 |

| 217 | Joe Rogan Experience | Los Angeles | Austin | HQ move | Read More | 2020 |

| 218 | JRS Company | Covina | Texas | HQ/manufacturing move | Read More | 2018 |

| 219 | Juul Labs | San Francisco | DC | HQ move | Read More | 2020 |

| 220 | Keen Horse Training | Arcadia | Texas | HQ move | Read More | 2020 |

| 221 | Kinwoven | San Diego | Oklahoma | HQ move | Read More | 2020 |

| 222 | Lockheed Martin FBM | Sunnyvale | Florida | HQ move | Read More | 2019 |

| 223 | Lucid Group | Newark | Arizona | EV manufacturing expansion | Read More | 2021 |

| 224 | Maxar Technologies | San Francisco | Colorado | HQ move | Read More | 2018 |

| 225 | Miro | San Francisco | Austin | Expansion | Read More | 2021 |

| 226 | Misfits Gaming Group | Los Angeles | Louisiana | HQ move | Read More | 2020 |

| 227 | Montrose Environmental Group | Irvine | Arkansas | HQ move | Read More | 2021 |

| 228 | Mullen Technologies | Brea | Tennessee | 1.2 million sf ev manufacturing expansion | Read More | 2021 |

| 229 | Mutual UFO Network (MUFON) | Los Angeles | Cincinnati | HQ move | Read More | 2021 |

| 230 | National Hot Rod Association | Glendora | Indiana | HQ move | Read More | 2021 |

| 231 | Nexen Tire | Diamond Bar | Ohio | HQ move | Read More | 2021 |

| 232 | Nintendo | Redwood City | Washington/British Columbia | Consolidation | Read More | 2021 |

| 233 | OKIN BPS | Mountain View | San Antonio | HQ move | Read More | 2018 |

| 234 | Old Gringo Boots | San Diego | Fort Worth | HQ move | Read More | 2021 |

| 235 | Optimal Elite Management LLC | Santa Clara | Austin | HQ/manufacturing move | Read More | 2020 |

| 236 | PerceptIn | Santa Clara | Indiana | HQ move | Read More | 2019 |

| 237 | Plumas Bancorp | Quincy | Reno | HQ move | Read More | 2021 |

| 238 | Premier Displays & Exhibits Inc. | Cypress | Las Vegas | HQ move | Read More | 2019 |

| 239 | Prenexus Health | Brawley | Arizona | HQ/manufacturing move | Read More | 2018 |

| 240 | Promises Behavioral Health | Long Beach | Tennessee | HQ move | Read More | 2019 |

| 241 | Puroast Coffee Co. Inc. | Woodland | North Carolina | HQ move | Read More | 2021 |

| 242 | QQE Summit LLC | Newark | Ohio | HQ move/manufacturing expansion | Read More | 2020 |

| 243 | Quetico, LLC | Chino | Arizona | HQ/logistics center move | Read More | 2019 |

| 244 | RaceChip | Brea | Florida | HQ move | Read More | 2019 |

| 245 | Regroup Mass Notification | San Francisco | Dallas | HQ move | Read More | 2020 |

| 246 | RiceBran Technologies | West Sacramento | Houston | HQ move | Read More | 2018 |

| 247 | Samsung (revised) | San Jose | Texas | $17 billion chip-making plant | Read More | 2021 |

| 248 | Scollar | Santa Rosa | Kansas City | HQ move | Read More | 2019 |

| 249 | Shmoop University, Inc. | Mountain View | Arizona | HQ move | Read More | 2019 |

| 250 | ShutterFly, Inc. (HQ2) | Redwood City | Minnesota | HQ2 | Read More | 2020 |

| 251 | Simwon America Corp. | Lathrop | Texas | EV parts manufacturing | Read More | 2021 |

| 252 | Smartrise Engineering | Sacramento | Texas | HQ move | Read More | 2018 |

| 253 | Smarty-Pits | Tehachapi | Oregon | HQ move | Read More | 2021 |

| 254 | Solvd Health | Carlsbad | Chicago | HQ move | Read More | 2021 |

| 255 | Space Channel Inc. | Los Angeles | Texas | HQ move | Read More | 2021 |

| 256 | Suzuki Marine USA | Brea | Florida | HQ move | Read More | 2021 |

| 257 | Synergy Blue | Palm Desert | Las Vegas | HQ move | Read More | 2019 |

| 258 | Tachyum | San Jose | Nevada | HQ move | Read More | 2020 |

| 259 | Tailift Material Handling USA | Ontario | Houston | HQ move | Read More | 2021 |

| 260 | TCS Healthcare Technologies | Auburn | North Carolina | HQ move | Read More | 2021 |

| 261 | theBalm | Alameda | Reno | HQ move and distribution facility expansion | Read More | 2020 |

| 262 | TV4 Entertainment | Venice | Florida | HQ move | Read More | 2019 |

| 263 | Unstoppable Domains | San Francisco | Reno | HQ move | Read More | 2020 |

| 264 | Upstart Network Inc. (HQ2) | San Carlos | Ohio | HQ2 | Read More | 2019 |

| 265 | UroDev Medical | San Clemente | Minnesota | HQ move | Read More | 2021 |

| 266 | Waterlogic USA, Inc. | Concord | Texas | HQ move | Read More | 2019 |

| 267 | Weatherby Inc. | Paso Robles | Wyoming | HQ/manufacturing move | Read More | 2019 |

| 268 | Weiss Watch Co. | Torrance | Nashville | HQ/manufacturing move | Read More | 2020 |

| 269 | William Glen Inc. | Sacramento | Texas | HQ move | Read More | 2021 |

| 270 | Woodward Inc. | Duarte | Colorado | HQ/manufacturing move | Read More | 2018 |

| 271 | Xos Inc. | Glassell Park | Tennessee | EV truck manufacturing; battery manufacturing | Read More | 2020 |

| 272 | Yeezy | Calabasas | Wyoming | HQ move | Read More | 2020 |

| 273 | Zeiss Vision Care | San Diego | Kentucky | HQ move | Read More | 2021 |

| Companies | From | To | Reason | Source | Year |

Employment 993k Below Recovery

EDD reported that employment (seasonally adjusted; September preliminary) was up 43,200 from the revised August numbers, while the number of unemployed was down by 12,800.

The reported unemployment rate was unchanged at 7.5% compared to 4.3% in February 2020 prior to the pandemic. California tied with Nevada for the highest unemployment rate among the states.

The national results again were somewhat stronger, with total US employment rising 526,000, and the number of unemployed dropping 710,000. The reported unemployment rate improved 0.4 point to 4.8%, compared to 3.5% in February 2020.

Figure Sources: California Employment Development Department; US Bureau of Labor Statistics

In the seasonally adjusted numbers, California employment remains 993,200 (5.3%) below the pre-pandemic level in February 2020; the rest of the states combined were 2.9% below. California was the 8th lowest ranked by employment recovery level, while 11 states were above the pre-pandemic February 2020 employment levels.

Labor Force Participation Rate

The labor force participation rate edged up 0.1 point to 61.1%, while the US number dipped by the same amount to 61.6%. The California rate remains well below the pre-pandemic level of 62.5%, which in turn was down substantially from prior years. Accounting for workers leaving the workforce since February 2020, there were 1.8 million out of work in September.

Nonfarm Jobs: 991k Below Recovery

Nonfarm wage and salary jobs were up 47,400 (seasonally adjusted) in September, while gains in August were revised down by 9,600.

Compared to the February 2020 numbers (seasonally adjusted) just prior to the pandemic, nonfarm wage and salary jobs in California were 991,000 short of recovery, or 19.9% of the national shortfall. California had the 13th lowest rate of job recovery.

In the seasonally adjusted numbers, two states—Utah and Idaho—continue to exceed the pre-pandemic levels, moving from recovery to growth.

Jobs Change by Industry

Using the unadjusted numbers that allow a more detailed look at industry shifts, 5 industries showed job levels at or exceeding the pre-pandemic February 2020 levels. The strongest lags in recovery continue to the those lower-wage industries that were hardest hit by the state-ordered closures: Arts, Entertainment & Recreation, Accommodation, Other Services, and Food Services. The relative levels of Government and Educational Services continue to be affected by seasonal factors as schools continued reopening in September, although some effect is likely coming from the drops in enrollment now being reported by the districts.

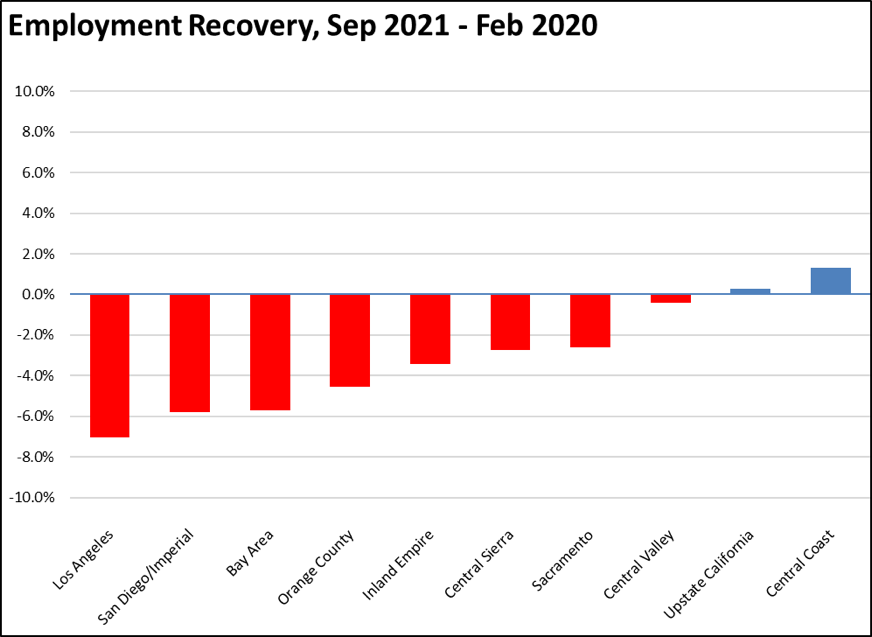

Employment Recovery by Region

Comparing September employment to pre-pandemic February 2020, Los Angeles Region lagged behind the rest of the state, showing a loss of 7.0% and containing 44% of the total employment shortfall in the state compared to 29% of the total population. Central Coast and Upstate California moved into the growth category.

Unemployment Rates by Legislative Districts

The highest and lowest estimated unemployment rates in September are shown below.

Lowest

| wdt_ID | Congressional District | Unemployment Rate |

|---|---|---|

| 2 | CD18 (Eshoo-D) | 3.0 |

| 3 | CD17 (Khanna-D) | 3.7 |

| 4 | CD02 (Huffman-D) | 4.1 |

| 5 | CD52 (Peters-D) | 4.1 |

| 6 | CD12 (Pelosi-D) | 3.8 |

| 7 | CD14 (Speier-D) | 3.9 |

| 9 | CD15 (Swalwell-D) | 4.1 |

| 10 | CD19 (Lofgren-D) | 4.3 |

| 12 | CD49 (Levin-D) | 4.3 |

| 13 | CD45 (Porter-D) | 4.3 |

| wdt_ID | Senate District | Unemployment Rate |

|---|---|---|

| 2 | SD13 (Hill-D) | 3.3 |

| 3 | SD15 (Beall-D) | 3.8 |

| 4 | SD11 (Wiener-D) | 4.0 |

| 5 | SD10 (Wieckowski-D) | 4.1 |

| 6 | SD36 (Bates-R) | 4.2 |

| 7 | SD01 (Dahle-R) | 4.5 |

| 8 | SD39 (Atkins-D) | 4.3 |

| 9 | SD02 (McGuire-D) | 4.4 |

| 10 | SD37 (Moorlach-R) | 4.3 |

| 11 | SD17 (Monning-D) | 4.9 |

| wdt_ID | Assembly District | Unemployment Rate |

|---|---|---|

| 2 | AD28 (Low-D) | 3.0 |

| 3 | AD24 (Berman-D) | 3.3 |

| 4 | AD22 (Mullin-D) | 3.3 |

| 5 | AD16 (Bauer-Kahan-D) | 3.6 |

| 6 | AD73 (Brough-R) | 4.0 |

| 7 | AD10 (Levine-D) | 4.0 |

| 8 | AD06 (Kiley-R) | 3.9 |

| 9 | AD25 (Chu-D) | 3.8 |

| 10 | AD17 (Chiu-D) | 3.8 |

| 11 | AD78 (Gloria-D) | 4.1 |

Highest

| wdt_ID | Congressional District | Unemployment Rate |

|---|---|---|

| 2 | CD29 (Cardenas-D) | 7.8 |

| 3 | CD37 (Bass-D) | 7.9 |

| 4 | CD28 (Schiff-D) | 8.0 |

| 5 | CD34 (Gomez-D) | 8.7 |

| 6 | CD16 (Costa-D) | 8.9 |

| 7 | CD32 (Napolitano-D) | 7.9 |

| 9 | CD21 (Cox-D) | 9.5 |

| 10 | CD40 (Roybal-Allard-D) | 9.5 |

| 12 | CD51 (Vargas-D) | 10.6 |

| 13 | CD44 (Barragan-D) | 10.6 |

| wdt_ID | Senate District | Unemployment Rate |

|---|---|---|

| 2 | SD22 (Rubio-D) | 7.1 |

| 3 | SD12 (Caballero-D) | 7.4 |

| 4 | SD21 (Wilk-R) | 8.5 |

| 5 | SD35 (Bradford-D) | 8.8 |

| 6 | SD24 (Durazo-D) | 8.8 |

| 7 | SD18 (Hertzberg-D) | 7.9 |

| 9 | SD30 (Mitchell-D) | 9.0 |

| 10 | SD33 (Gonzalez-D) | 9.1 |

| 12 | SD40 (Hueso-D) | 9.4 |

| 13 | SD14 (Hurtado-D) | 10.4 |

| wdt_ID | Assembly District | Unemployment Rate |

|---|---|---|

| 2 | AD46 (Nazarian-D) | 8.8 |

| 3 | AD31 (Arambula-D) | 9.3 |

| 4 | AD36 (Lackey-R) | 9.2 |

| 5 | AD63 (Rendon-D) | 9.8 |

| 6 | AD32 (Salas-D) | 9.6 |

| 7 | AD26 (Mathis-R) | 9.0 |

| 9 | AD51 (Carrillo-D) | 9.9 |

| 10 | AD64 (Gipson-D) | 10.3 |

| 12 | AD59 (Jones-Sawyer-D) | 10.4 |

| 13 | AD56 (Garcia-D) | 11.3 |

Unemployment Rates by Region

Unemployment rates (not seasonally adjusted) compared to pre-pandemic February 2020 show Los Angeles Region moving up to the second worst outcome in the state.

| wdt_ID | Region | September - 21 | Feb - 20 |

|---|---|---|---|

| 2 | California | 6.4 | 4.3 |

| 6 | Bay Area | 4.6 | 2.7 |

| 10 | Orange County | 5.0 | 7.0 |

| 14 | Central Coast | 5.3 | 4.6 |

| 18 | Sacramento | 5.5 | 4.5 |

| 22 | Central Sierra | 5.5 | 8.4 |

| 26 | Upstate California | 5.9 | 2.8 |

| 30 | San Diego/Imperial | 6.1 | 3.9 |

| 34 | Inland Empire | 6.6 | 3.7 |

| 38 | Los Angeles | 7.9 | 6.3 |

| 39 | Central Valley | 8.0 | 3.8 |

Figure Source: California Employment Development Department

MSAs with the Worst Unemployment Rates

California had 11 of the MSAs among the 25 regions with the worst unemployment rates in August.

| wdt_ID | MSA | August Unemployment Rate | US Rank out of 389 |

|---|---|---|---|

| 1 | El Centro MSA | 18.1 | 389 |

| 2 | Visalia-Porterville MSA | 9.3 | 387 |

| 3 | Bakersfield MSA | 8.7 | 385 |

| 4 | Merced MSA | 8.2 | 384 |

| 5 | Hanford-Corcoran MSA | 8.0 | 380 |

| 6 | Fresno MSA | 7.8 | 379 |

| 7 | Stockton-Lodi MSA | 7.5 | 376 |

| 8 | Los Angeles-Long Beach-Anaheim MSA | 7.4 | 374 |

| 9 | Madera MSA | 7.3 | 372 |

| 10 | Yuba City MSA | 7.2 | 371 |

| 11 | Modesto MSA | 6.9 | 365 |